TL;DR: Wire Transfers

A wire transfer is an electronic payment method that moves funds directly between bank accounts. It is characterized by its speed (often same-day) and finality, as the transaction is generally irrevocable once accepted by the receiving bank.

Key Takeaways

-

The Model: Transfers use secure messaging networks like Fedwire (domestic US) or SWIFT (international). Domestic wires typically settle within hours, while international transfers involve intermediary banks and take 1–5 business days.

-

Ideal Context: Essential for high-value B2B payments, real estate closings, and international supplier settlements where immediate funds availability and payment certainty are required.

-

Implementation Steps:

-

Gather Recipient Data: Collect the legal name, account number, and routing number (domestic) or SWIFT/BIC/IBAN (international).

-

Verify Instructions: Always confirm wire details via a secondary “out-of-band” method (like a phone call) to prevent invoice fraud.

-

Initiate Before Cutoff: Submit transfers before the bank’s daily deadline (typically 3:00–5:00 PM ET) to ensure same-day processing.

-

Factor in Fees: Account for outgoing fees ($15–$50) and potential intermediary bank deductions that can cause payment mismatches.

-

-

Billing Tech: AR automation platforms simplify wire acceptance by automatically matching incoming funds to open invoices, reducing the manual effort of “cash application.”

The Bottom Line

While wire transfers are more expensive than ACH, they are the gold standard for security and speed in enterprise transactions. For businesses scaling globally, mastering wire workflows is the key to ensuring reliable cross-border payments and maintaining strong vendor relationships.

Are you looking to reduce the manual work of reconciling incoming wires, or do you need help setting up secure dual-authorization protocols for outgoing transfers?

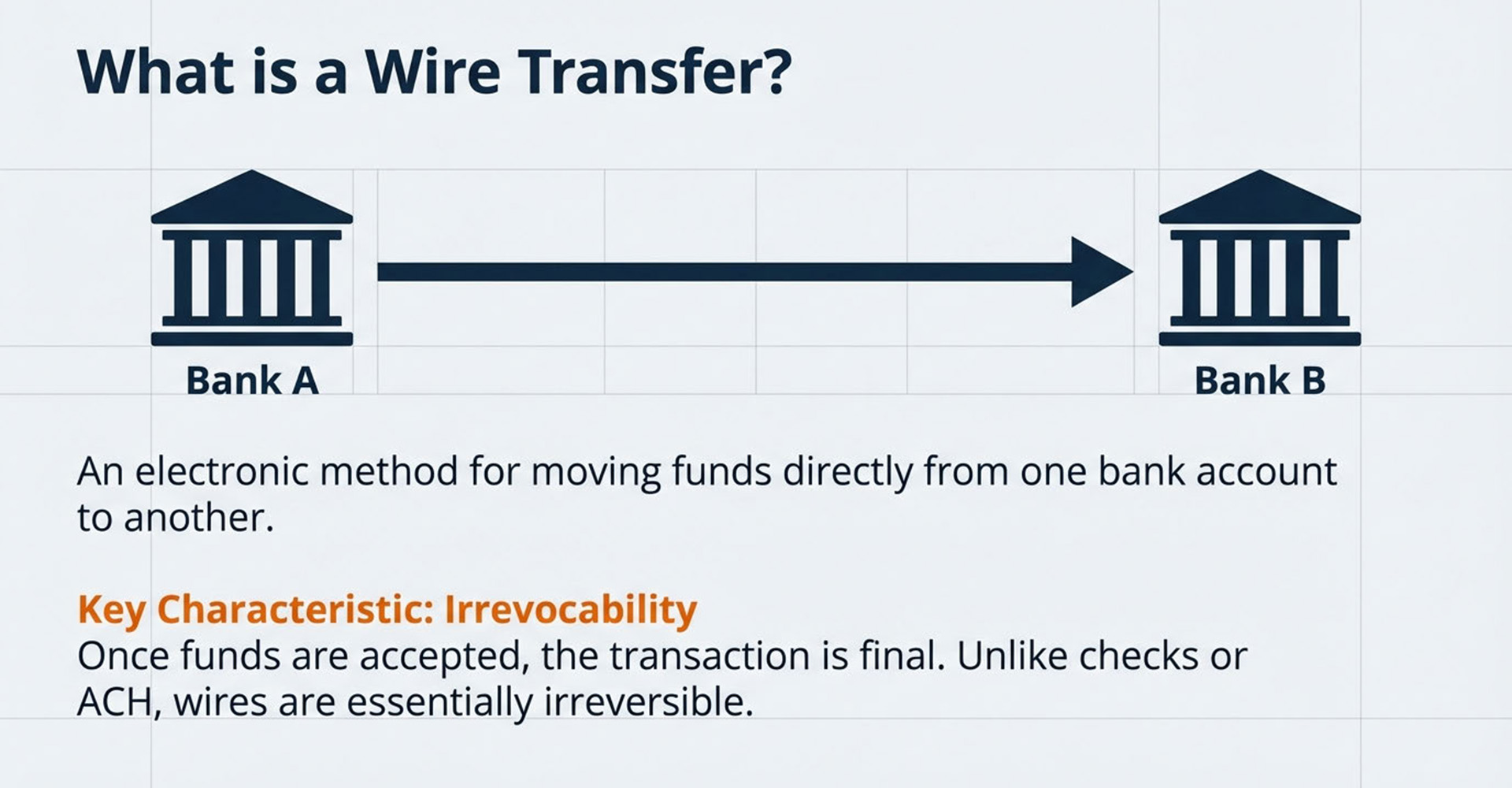

A wire transfer is an electronic payment method that moves funds directly from one bank account to another, typically completing within the same day for domestic transactions or one to five business days for international transfers. Unlike ACH payments or checks, wire transfers are generally irrevocable once the receiving bank accepts the funds.

This guide covers how wire transfers work, what they cost, how long they take, and when they make sense compared to other payment methods.

What is a wire transfer

What is a wire transfer and why do businesses use it?

A wire transfer is an electronic method for moving funds directly from one bank account to another. Domestic transfers within the United States typically arrive the same day when initiated before bank cutoff times, while international transfers take one to five business days. Fees generally range from $0 to $50, with cross-border transactions costing more.

What makes wire transfers distinct from other payment methods is their finality. Once the receiving bank accepts the funds, the transaction is essentially irreversible. This characteristic makes wires particularly useful for large, time-sensitive payments where both parties want certainty that the money cannot be clawed back.

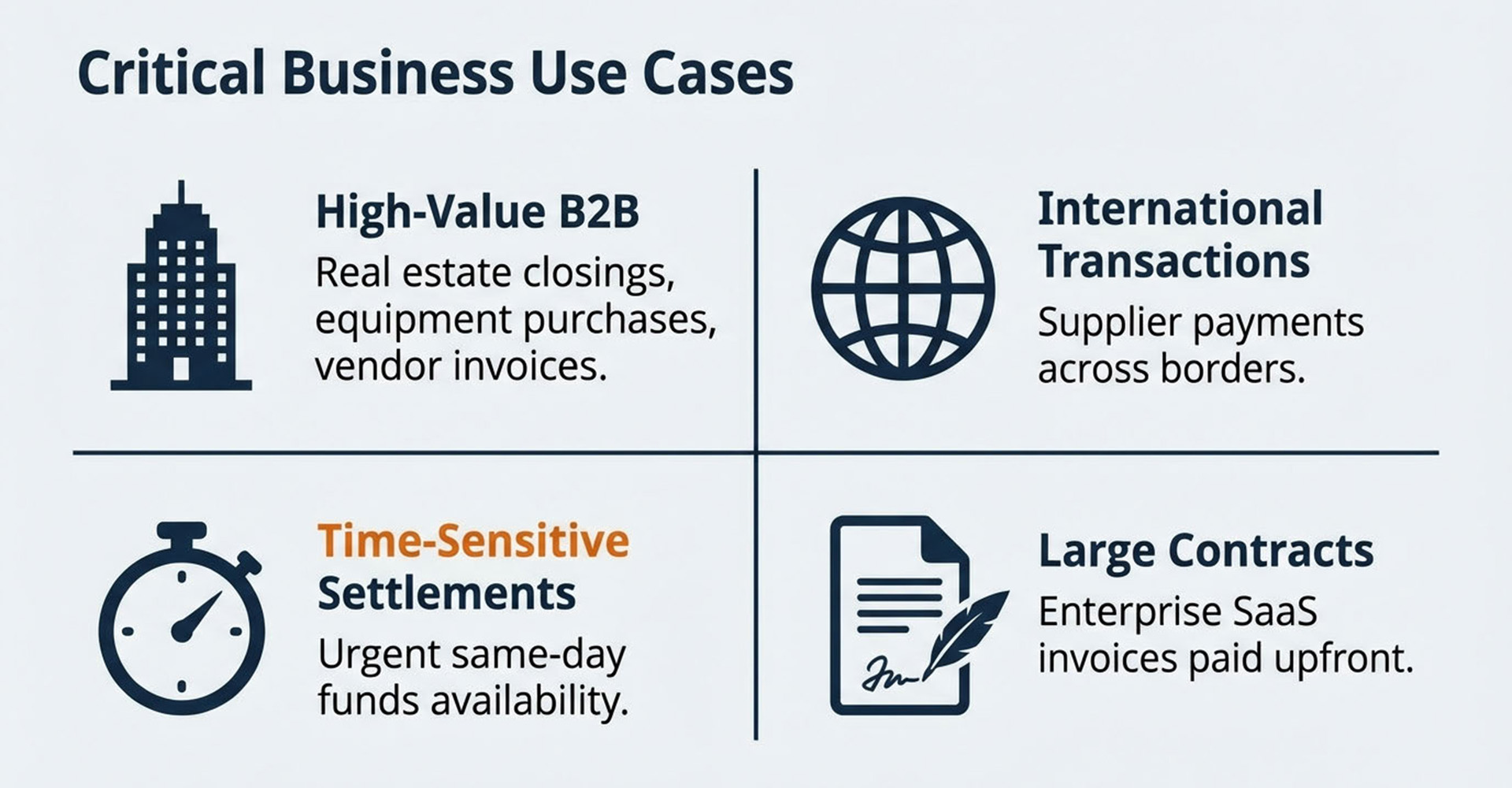

Businesses commonly rely on wire transfers for:

- High-value B2B payments: Vendor invoices, real estate closings, and equipment purchases

- International transactions: Paying suppliers or partners in other countries

- Time-sensitive settlements: When same-day funds availability is critical

- Large subscription contracts: Enterprise customers paying annual SaaS invoices upfront

How Wire Transfers Work

How does a wire transfer move money from one account to another?

Wire transfers use secure interbank messaging networks to transmit payment instructions between financial institutions. In the United States, domestic wires travel through Fedwire, the Federal Reserve’s real-time settlement system. International wires use the SWIFT network, which connects over 11,000 financial institutions worldwide.

- Initiation by the sender

The sender provides their bank with the recipient’s details and authorizes the transfer. This can happen through online banking, a mobile app, or an in-person branch visit. At this stage, the sender specifies the amount, recipient information, and which account to draw from.

- Verification and processing

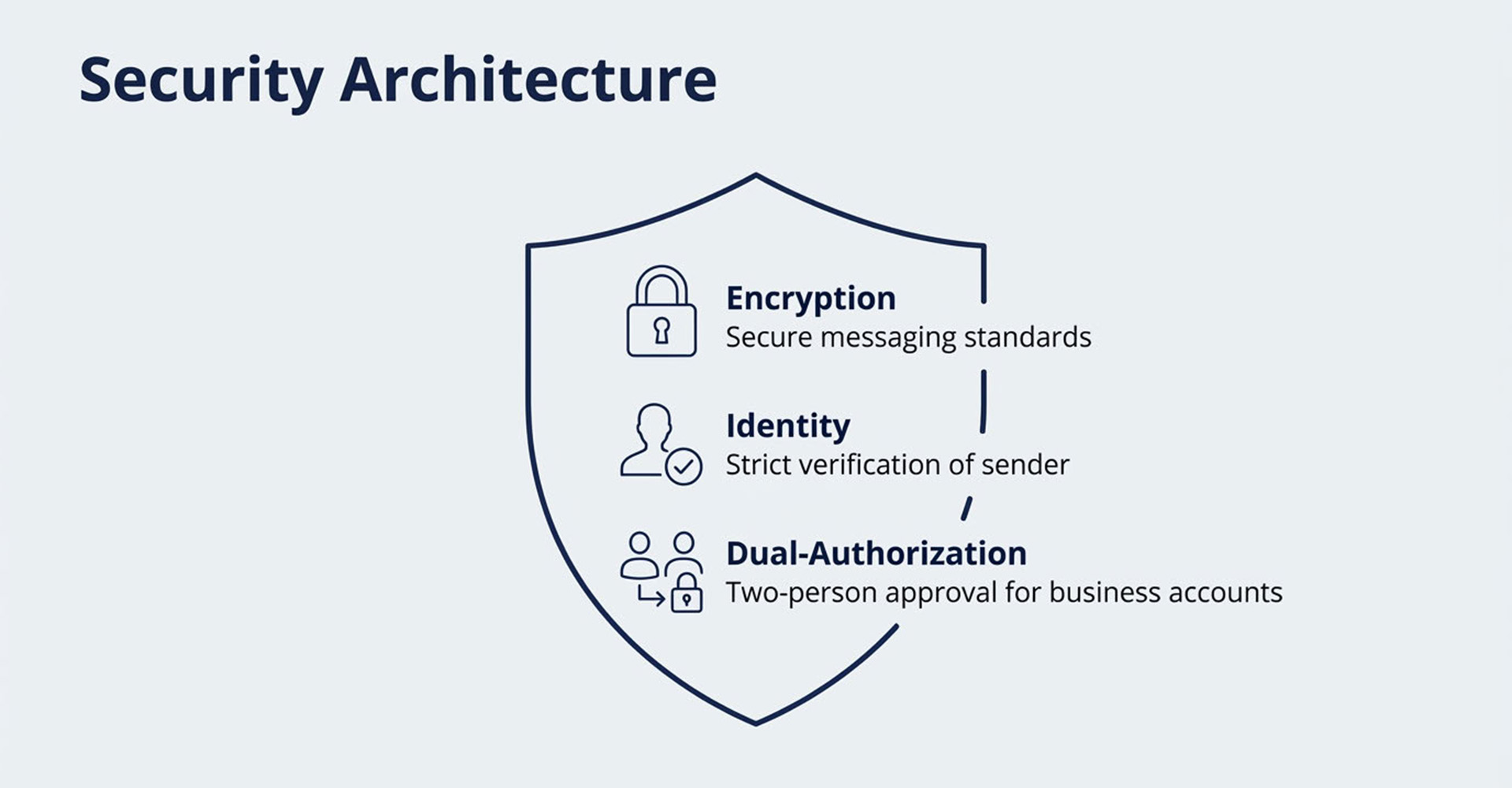

Next, the sending bank verifies that sufficient funds exist and authenticates the request. For business accounts, this step often includes dual-authorization controls, consistent with SOX compliance requirements, where a second person approves the transfer before it proceeds.

- Transmission through banking networks

Once approved, the sending bank transmits instructions through the appropriate network. Domestic US wires use Fedwire for same-day settlement, while international wires route through SWIFT. Cross-border transfers may pass through one or more intermediary banks before reaching the destination, though 86% of SWIFT payments involve one or no intermediaries.

- Receipt and crediting to recipient

Finally, the receiving bank processes the incoming instructions and credits the recipient’s account. For domestic wires, funds are typically available immediately. International transfers may require additional processing time for currency conversion and compliance checks.

How to Wire Money Step by Step

How do you wire money from your bank account?

Sending a wire transfer requires gathering specific information about the recipient and their bank beforehand. Missing or incorrect details can delay the transfer or cause it to fail entirely.

Information required to send a wire transfer

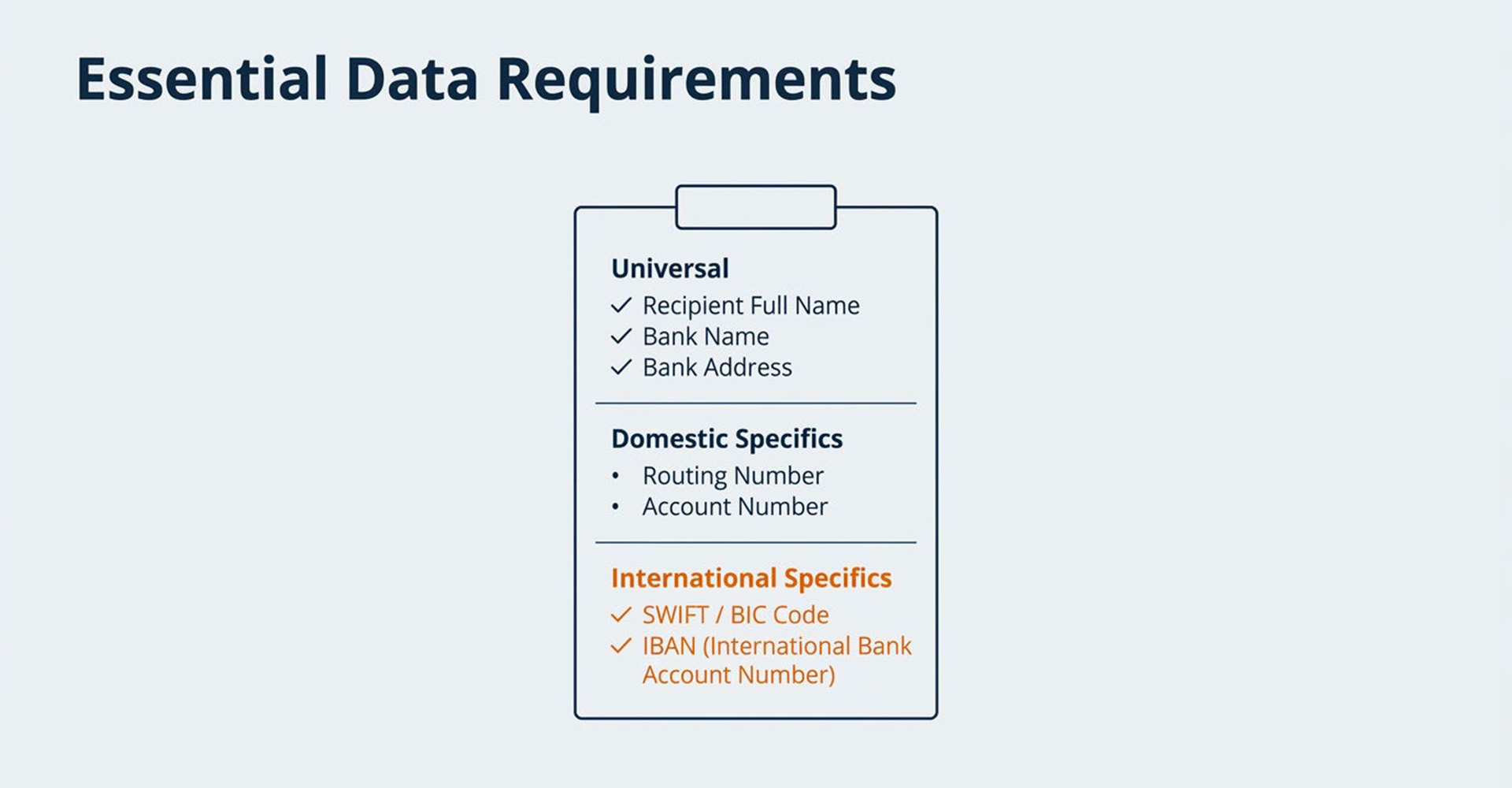

Before initiating a wire, you’ll want to collect the following from your recipient:

- Recipient’s full legal name (as it appears on their bank account)

- Recipient’s bank name and address

- Recipient’s bank account number

- Routing number (for domestic transfers) or SWIFT/BIC code (for international)

- IBAN (required for transfers to many countries, particularly in Europe)

- Purpose of transfer (sometimes required for compliance documentation)

How to send a domestic wire transfer

For transfers within the United States, log into your bank’s online platform or mobile app and navigate to the wire transfer section. Enter the recipient’s routing number and account number, specify the amount, and review all details carefully before confirming. Most banks process domestic wires initiated before 3:00–5:00 PM Eastern time on the same business day.

How to send an international wire transfer

International wires require additional information, including the recipient bank’s SWIFT code and potentially an intermediary bank’s details. You’ll also select the currency for the transfer, either sending in US dollars or converting to the recipient’s local currency. Exchange rates and additional fees apply, so it’s worth reviewing the total cost before confirming.

How to Receive a Wire Transfer

What do you need to receive a wire transfer?

Receiving a wire transfer is straightforward once you provide the sender with your banking details. The recipient’s role is primarily informational.

Bank details needed to receive a wire

Provide the sender with your full legal name as it appears on your account, your bank’s name and address, your account number, and your bank’s routing number (domestic) or SWIFT code (international). Some banks also require intermediary bank information for international transfers.

Receiving domestic wire transfers

Domestic wires typically credit to your account the same day they’re sent, assuming the sender initiated the transfer during business hours. Your bank may charge an incoming wire fee, which is usually deducted from the transfer amount or charged separately.

Receiving international wire transfers

International wires take longer due to time zone differences and the involvement of correspondent banks. Currency conversion happens automatically if the sender wired funds in a foreign currency. Be aware that intermediary banks may deduct fees from the transfer amount before it reaches you.

Wire Transfer Costs and Fees

How much does a wire transfer cost?

Wire transfer fees vary by bank, transfer direction, and whether the transaction is domestic or international. Both senders and recipients may incur charges.

INSERT TABLE

Outgoing wire transfer fees

Senders pay a flat fee to initiate wire transfers. Domestic wires typically cost $15–$30, while international wires range from $35–$50 or more depending on the destination country.

Incoming wire transfer fees

Some banks charge recipients a fee to receive wire transfers, typically $0–$15 for domestic wires and up to $25 for international.

Intermediary bank fees

International wires often route through correspondent banks that facilitate the transfer between sending and receiving institutions. Each intermediary may deduct a fee from the transfer amount, reducing what the recipient ultimately receives. For SaaS businesses, these deductions are a frequent reason payments don’t match invoices.

Foreign exchange and currency conversion costs

When a wire crosses currencies, banks apply an exchange rate that includes a markup over the mid-market rate. This foreign exchange spread typically adds 1%–3% to the transaction cost.

How Long Does a Wire Transfer Take

How long does it take for a wire transfer to arrive?

Transfer timing depends primarily on whether the wire is domestic or international, and when during the business day it’s initiated.

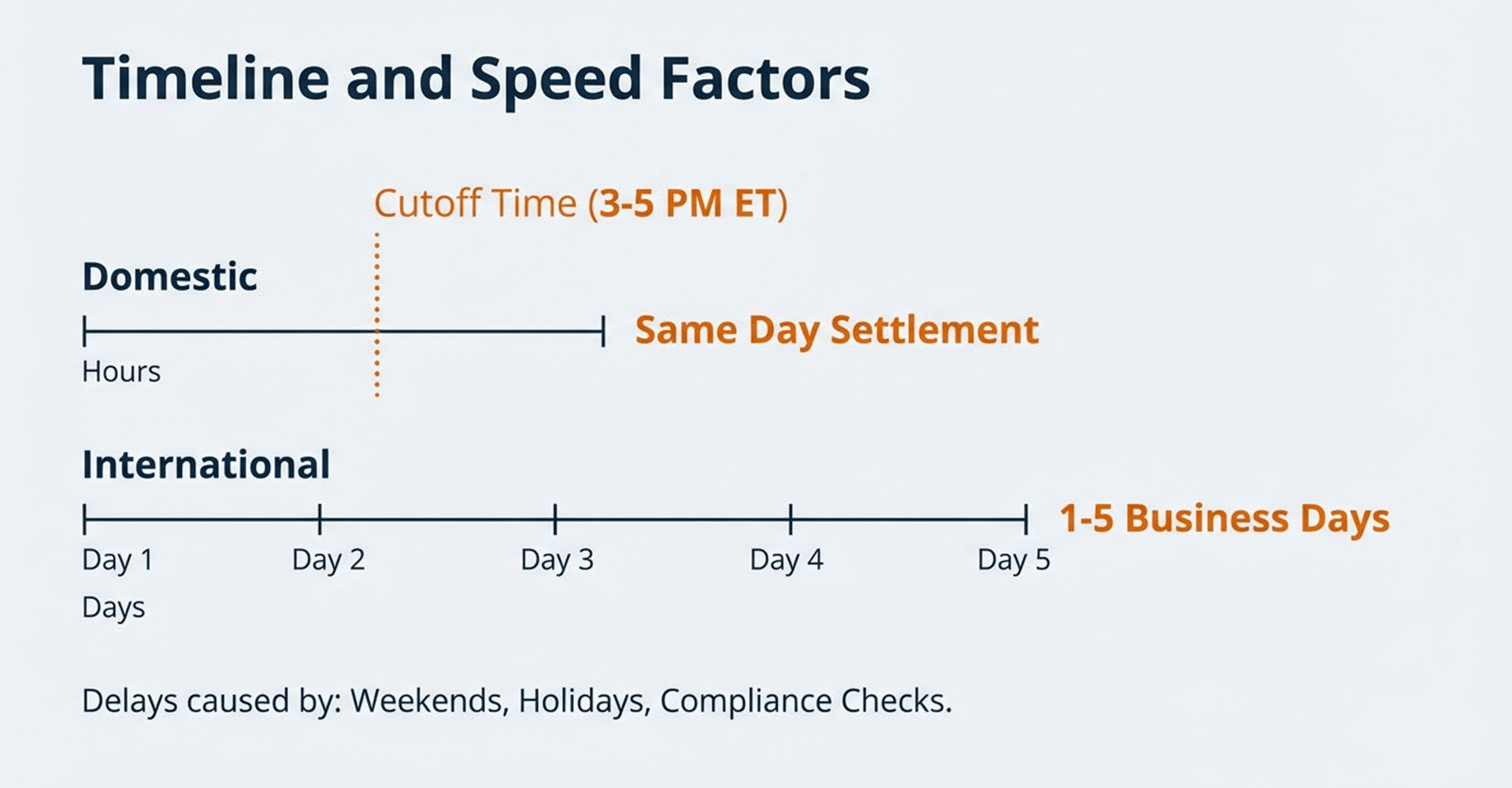

Domestic wire transfer timeline

Domestic wire transfers in the United States typically complete the same business day if initiated before your bank’s cutoff time, usually 3:00–5:00 PM Eastern. Transfers sent after the cutoff process the next business day.

International wire transfer timeline

International wires generally take one to five business days, depending on the destination country, currencies involved, and number of intermediary banks in the payment chain.

Factors that affect wire transfer speed

- Time of initiation: Transfers sent after cutoff times process the next business day

- Weekends and holidays: Banks do not process wires on non-business days

- Intermediary banks: Each additional bank in the chain adds processing time

- Compliance reviews: Large or unusual transfers may trigger additional verification

Domestic Wire Transfer Meaning and How it Differs from International Transfers

What is a domestic wire transfer and how does it differ from an international wire?

A domestic wire transfer moves funds between two bank accounts within the same country. In the United States, domestic wires use the Fedwire system and typically settle within hours. International wire transfers cross national borders and use the SWIFT network, involving more complexity and longer processing times.

INSERT TABLE

Wire Transfer Security and Fraud Prevention

Are wire transfers secure?

Wire transfers are among the most secure payment methods available, with multiple layers of verification and encrypted transmission. However, their irrevocable nature makes them attractive targets for fraud.

Why wire transfers are secure

Banks verify sender identity through authentication protocols before processing wire requests. The interbank networks use encryption and secure messaging standards. Many business accounts require dual authorization, where two people approve transfers above certain thresholds.

Common wire transfer scams to avoid

- Business email compromise: Criminals impersonate executives or vendors, requesting urgent wire transfers to fraudulent accounts — 73% of all reported cyber incidents in 2024 according to the Federal Reserve

- Invoice fraud: Fake invoices arrive with altered wire instructions, redirecting legitimate payments

- Real estate scams: Fraudulent closing instructions sent to homebuyers, often intercepting email communications, with FBI IC3 reporting a 72% increase in victim losses from real estate BEC scams between 2020 and 2022

How to Protect Your Business from Wire Fraud

Verify wire instructions by phone using a known number rather than contact information from the wire request itself. Implement dual-authorization requirements for transfers above a set threshold. Train staff to recognize phishing attempts and confirm any changes to vendor payment details directly with a known contact.

Bank Transfer and Wire Transfer Compared to Other Payment Methods

When is a wire transfer the right choice versus other payment methods?

Wire transfers excel for large, time-sensitive payments but aren’t always the most cost-effective option.

Wire transfer vs ACH transfer

ACH (Automated Clearing House) transfers move funds between US bank accounts through batch processing, typically taking one to three business days. ACH costs significantly less than wire transfers and is commonly used for recurring ACH payments like subscriptions and payroll, but it lacks same-day settlement for most transactions. Unlike wires, ACH payments can sometimes be reversed.

Wire transfer vs Zelle and digital wallets

Zelle and similar services are not wire transfers. They use different networks designed for smaller, person-to-person payments with transaction limits that make them unsuitable for most business payments.

When to use wire transfers for B2B payments

Wire transfers make sense when payment amounts exceed ACH limits or when credit card surcharges on high-value transactions make cards impractical, when same-day settlement is required, when paying international vendors, or when enterprise customers prefer wiring large annual subscription payments.

INSERT TABLE

Best Practices for Businesses Accepting Wire Transfers

How can businesses efficiently accept and process wire transfer payments?

For B2B companies that receive wire payments regularly, operational efficiency depends on clear communication and streamlined reconciliation.

- Provide clear wire instructions: Include all required details on invoices to prevent errors and delays

- Track incoming wires: Reconcile wire receipts against outstanding invoices daily

- Automate cash application: Manual matching of wire payments to invoices is time-consuming and error-prone

- Offer multiple payment options: Give customers flexibility to pay via wire, ACH, or credit card

- Communicate fees: Be transparent about whether your business absorbs incoming wire fees or expects customers to cover them

Simplify Wire Transfer Payment Collection with Automated AR

How can automation reduce the manual work of processing wire transfer payments?

Businesses receiving frequent wire payments often struggle with manual reconciliation. Matching incoming wires to open invoices, updating customer balances, and posting journal entries consumes hours of staff time each month, directly extending the month-end close.

AR automation platforms can match incoming wire payments to invoices automatically, update customer account balances in real time, and post the corresponding journal entries to your general ledger. Ordway’s Accounts Receivable Automation solution supports multiple payment methods including wires, ACH, and cards, with automated cash application and reconciliation built in.

Frequently Asked Questions

Can you cancel a wire transfer after it has been sent?

Wire transfers are generally irrevocable once processed. However, contacting your bank immediately after initiating the transfer may allow cancellation if the funds haven’t yet left your account. Once the receiving bank accepts the funds, recovery becomes extremely difficult.

Is there a maximum dollar amount you can send through a wire transfer?

There is no regulatory maximum for wire transfer amounts. However, individual banks may impose daily or per-transaction limits, particularly for online-initiated transfers.

Do banks process wire transfers on holidays and weekends?

No. Wire transfers are only processed on business days when banks and the Federal Reserve are open. Transfers initiated on weekends or bank holidays will not be completed until the next business day.