TL;DR: Bank Identifier Code (BIC)

A Bank Identifier Code (BIC) is an 8 to 11-character alphanumeric code used to uniquely identify a specific financial institution globally. It serves as a “postal code” for banks, ensuring international wire transfers and SEPA payments reach the correct destination.

Key Takeaways

-

The Model: While the IBAN identifies a specific account, the BIC/SWIFT code identifies the bank itself. Both are typically required for cross-border transactions to prevent misrouting.

-

Ideal Context: Mandatory for international wire transfers, SEPA payments in Europe, and global B2B transactions.

-

Implementation Steps:

-

Verify Structure: A standard BIC includes a 4-letter bank code, a 2-letter country code, a 2-character location code, and an optional 3-character branch code.

-

Locate Details: Find your BIC on monthly bank statements, within your online banking portal, or via official SWIFT lookup tools.

-

Domestic Exception: If you are conducting domestic transfers within the US, use a 9-digit ABA routing number instead of a BIC.

-

Billing Tech: High-growth SaaS companies use automated billing platforms to validate BICs in real-time, reducing failed payments and manual reconciliation.

-

The Bottom Line

The BIC is the essential “address” for global banking. For businesses operating internationally, accurate BIC usage is the foundation for automated payment processing, lower rejection fees, and a friction-free customer experience.

Are you looking to automate the validation of BIC codes for your international customers, or are you comparing different methods for cross-border payment routing?

A Bank Identifier Code (BIC) is an 8 to 11-character alphanumeric code that uniquely identifies a specific bank or branch worldwide. It’s the global standard for routing international wire transfers and SEPA payments, ensuring funds reach the correct financial institution. This guide covers how BIC codes are structured, where to find yours, when you’ll need one, and how BIC codes relate to IBANs and routing numbers.

What is a Bank Identifier Code

What is a BIC code and why does it matter for international payments?

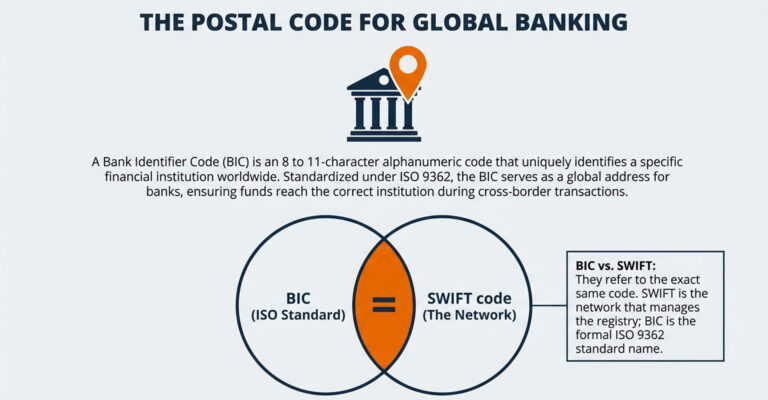

A Bank Identifier Code (BIC) is an 8 to 11-character alphanumeric code that uniquely identifies a specific financial institution worldwide. Standardized under ISO 9362, the BIC serves as a global address for banks, ensuring funds reach the correct institution during cross-border transactions. You’ll encounter BIC codes whenever you send or receive international wire transfers, SEPA payments in Europe, or cross-border business payments.

Think of the BIC as a postal code for banks. Without it, your payment could end up delayed, returned, or misrouted entirely. Every bank participating in international transfers has at least one BIC assigned to it, and larger institutions often have multiple codes for different branches or departments. BIC stands for Bank Identifier Code, though it was formerly known as Bank Identification Code. You might also see it called a SWIFT code, which we’ll cover next.

Is a BIC code the same as a SWIFT code?

What is the difference between a BIC code and a SWIFT code?

BIC and SWIFT code refer to the exact same identifier. The Society for Worldwide Interbank Financial Telecommunication (SWIFT) manages the BIC registry and operates the messaging network used for international payments. Because SWIFT assigns and maintains the codes, the terms have become interchangeable.

- BIC: The formal ISO standard name for the code

- SWIFT code: The common name derived from the network that manages BIC codes

When your bank asks for a SWIFT code, they’re asking for the BIC. When a vendor requests your BIC, they want your SWIFT code. Both terms appear on bank documents, and neither is incorrect.

BIC code structure and format

How is a BIC/SWIFT code structured?

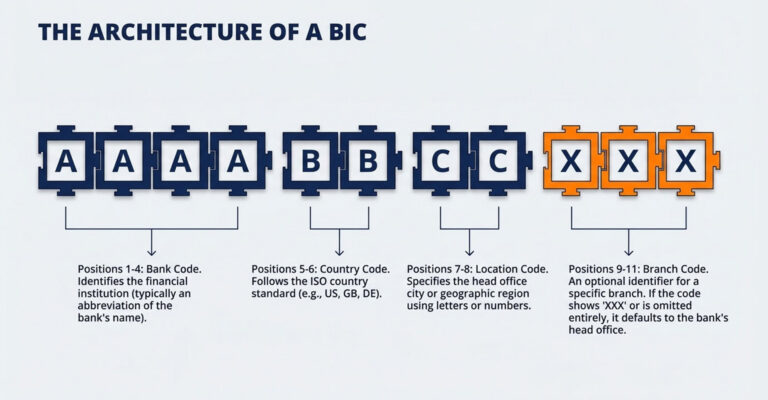

Every BIC follows a standardized format that becomes readable once you understand the pattern. The code is either 8 or 11 characters long, structured as AAAABBCCXXX.

| Position | Characters | Description |

|---|---|---|

| 1–4 | AAAA | Bank code |

| 5–6 | BB | Country code |

| 7–8 | CC | Location code |

| 9–11 | XXX | Branch code (optional) |

Bank code

The first four letters identify the financial institution. This is typically an abbreviated version of the bank’s name. For example, CHAS represents JPMorgan Chase, while DEUT represents Deutsche Bank.

Country code

The next two letters follow the ISO country code standard, indicating where the bank is registered. US represents the United States, GB represents the United Kingdom, and DE represents Germany.

Location code

The following two alphanumeric characters specify the bank’s head office city or region. Location codes can include both letters and numbers, providing geographic precision within the country.

Branch code

The final three characters are optional and identify a specific branch. If the code shows XXX or is omitted entirely, it refers to the bank’s head office. An 8-character BIC defaults to the primary office, while an 11-character BIC can route payments to a particular branch.

BIC code example

What does a real BIC code look like?

Let’s break down an actual BIC to see how the structure works in practice. The BIC for JPMorgan Chase is CHASUS33XXX.

- CHAS: Bank code for JPMorgan Chase

- US: Country code for United States

- 33: Location code for New York

- XXX: Head office indicator

The 8-character version, CHASUS33, refers to the head office and works for most transfers. The 11-character version allows you to specify a particular branch when needed, though many banks route payments correctly with just the shorter code.

How to find your bank BIC code

How do I find my bank identification code?

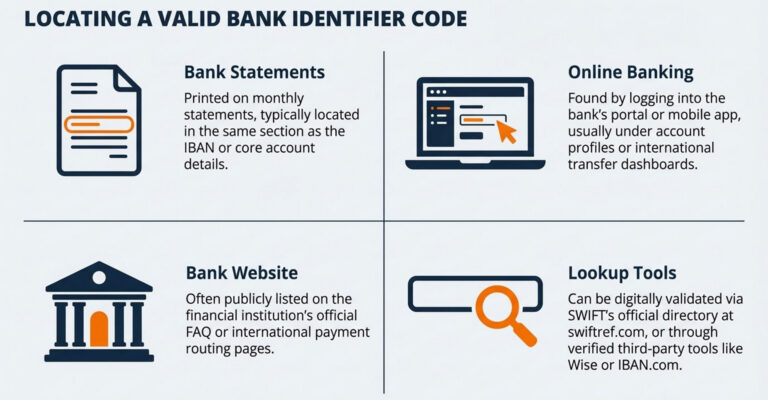

Locating your BIC is straightforward. You have several options depending on what’s most convenient.

On bank statements

Your monthly bank statements typically display the BIC/SWIFT code alongside your other account details. Look near the sections showing your IBAN or account number. The BIC is usually printed in the same area.

Through online banking

Log into your bank’s online portal or mobile app. You can usually find the BIC under account details, your profile settings, or in the international transfer section. Some banks display it prominently on the dashboard.

On your bank website

Many banks list their BIC codes on their FAQ or international payments pages. A quick search for “[bank name] BIC code” often provides direct results from the bank’s official site.

Using a BIC lookup tool

Online SWIFT/BIC finders allow you to search by bank name, country, or city. SWIFT’s official directory at swiftref.com offers a reliable lookup, and third-party tools from Wise or IBAN.com provide similar functionality.

When you need a BIC code

When is a BIC code required?

BIC codes become essential whenever the sending bank identifies the receiving financial institution across borders.

International wire transfers

A BIC is required for sending or receiving money across borders via wire transfer. The BIC ensures that intermediary and beneficiary banks are correctly identified throughout the payment chain, even when multiple correspondent banks are involved.

SEPA payments in Europe

Transactions within the Single Euro Payments Area require a BIC alongside an IBAN for euro-denominated transfers between participating countries. While some SEPA transfers can now proceed with just an IBAN, many banks still request the BIC for verification.

Cross-border business payments

B2B payments to international vendors, suppliers, or partners require accurate BIC codes to prevent misrouting and delays. This is especially relevant for companies with global payment operations processing invoices across multiple currencies and jurisdictions.

How BIC codes work in international payments

How does a BIC code facilitate international payments?

The BIC code acts as a precise address, guiding a payment through the global banking network. Here’s how the process typically unfolds:

- Step 1: The sender initiates an international transfer, providing the recipient’s BIC and IBAN (or account number)

- Step 2: The sending bank uses the BIC to identify the recipient’s bank on the SWIFT network

- Step 3: A SWIFT message containing the payment instructions is transmitted, sometimes routing through correspondent (intermediary) banks

- Step 4: The recipient’s bank receives the funds and credits the correct account

The BIC ensures the payment message reaches the correct financial institution anywhere in the world. Without it, the sending bank would have no standardized way to identify where the funds belong.

Are there fees for using BIC codes

Does using a BIC code cost money?

The BIC code itself is free to use. There’s no charge for the code. However, the international wire transfers that require a BIC do incur fees from sending, intermediary, and receiving banks. Fees vary depending on the bank, transfer amount, and destination country. Some payment methods, like SEPA direct debits within Europe, typically have lower fees than traditional wire transfers. It’s worth checking with your bank about fee structures before initiating international payments.

BIC vs IBAN vs Routing Number

What is the difference between a BIC, IBAN, and routing number?

BIC, IBAN, and routing numbers serve complementary but distinct purposes in the banking system.

| Identifier | Purpose | Format | Usage |

|---|---|---|---|

| BIC | Identifies the bank | 8–11 characters | International transfers |

| IBAN | Identifies the specific account | Up to 34 characters | International transfers (primarily Europe) |

| Routing Number | Identifies a US bank | 9 digits | Domestic US transfers (ACH, wire) |

International transfers typically require both a BIC and an IBAN. US domestic transfers use routing numbers instead. If you’re sending money from the US to Europe, you’ll provide the recipient’s BIC and IBAN. If you’re receiving a domestic ACH payment, you’ll share your routing number and account number.

BIC codes for Business and Recurring Payments

How do BIC codes affect business payment operations?

Businesses that process international invoices, vendor payments, or customer collections manage BIC data across their operations. The complexity increases with scale.

- Vendor payments: Paying international suppliers requires their bank’s BIC to ensure payment arrives without delays

- Customer collections: Receiving payments from global customers via wire transfer or direct debit often requires collecting their BIC during onboarding

- Recurring billing: Subscription businesses collecting from international customers may require the BIC for certain payment methods, particularly SEPA direct debits in Europe

Billing platforms that handle multi-currency payments typically manage BIC data as part of the customer payment profile. For companies scaling internationally, automating data collection and validation becomes increasingly important.

Why BIC Code Accuracy Matters for Payment Automation

What happens when BIC codes are incorrect in automated payment systems?

Errors in BIC codes can lead to significant operational issues that compound over time:

- Delayed payments: Incorrect codes cause transfers to be returned, requiring re-processing and extending payment timelines

- Failed transactions: Payments may be rejected entirely by the banking network, leaving invoices unpaid

- Manual intervention: Staff spend time researching and correcting errors, increasing operational costs

- Customer friction: Billing disputes and poor customer experiences arise from payment failures

For companies automating accounts receivable and recurring payment collection, validating payment details reduces failed transactions and accelerates cash flow. This is particularly relevant for subscription businesses where payment failures can trigger involuntary churn. When onboarding international customers, validate BIC codes at the point of collection rather than discovering errors during payment processing. Many billing platforms offer real-time BIC validation to catch issues early. Ordway’s payment automation capabilities help subscription businesses handle the complexities of international payments, including multi-currency billing and automated payment collection across global bank transfers.

Frequently Asked Questions

What happens if I enter the wrong BIC code?

The payment may be delayed, returned, or in rare cases, sent to the wrong financial institution. Contact your bank immediately to recall or correct the transfer. Most banks can intervene if you catch the error quickly, though fees may apply for the correction.

Can a bank have multiple BIC codes?

Yes. Large banks often have different BIC codes for different branches, departments (like foreign exchange or securities), or countries of operation. When in doubt, confirm the correct BIC with the recipient or their bank.

Do I need a BIC code for domestic transfers within the United States?

No. Domestic transfers within the US use 9-digit ABA routing numbers. BIC codes are only required for international transactions. If you’re sending money to another US bank account, you’ll use the routing number and account number instead.

How do I validate a BIC code before sending an international payment?

You can use SWIFT’s official BIC directory or a reputable online validator to confirm the code matches the intended bank and branch before initiating a payment. This simple step can prevent costly delays and failed transactions.

What is the difference between an 8-character and 11-character BIC code?

An 8-character BIC identifies the bank’s head or primary office, while an 11-character BIC specifies a particular branch. Both are valid for transfers, but using the 11-character code can ensure faster routing to a specific branch when that level of precision matters.