TL;DR: International Bank Account Number (IBAN)

An International Bank Account Number (IBAN) is a standardized alphanumeric code (up to 34 characters) used to identify specific bank accounts for cross-border transfers. It eliminates errors and delays by wrapping country, bank, and account details into a single, globally recognized format.

Key Takeaways

-

The Model: The IBAN identifies the specific account, while a SWIFT/BIC code identifies the bank institution. Most international transfers require both.

-

Ideal Context: Mandatory for transfers within the SEPA zone (Europe) and widely used in the Middle East and parts of Africa/Caribbean.

-

Implementation Steps:

-

Verify Structure: Ensure the code includes the two-letter Country Code, two Check Digits (for mathematical validation), and the Basic Bank Account Number (BBAN).

-

Locate Details: Find your IBAN on bank statements, mobile apps, or through your bank’s customer service.

-

Cross-Border Coordination: If billing US customers, remember that US banks do not use IBANs; you must use a routing number and SWIFT code instead.

-

-

Billing Tech: Recurring billing platforms can automate the collection of IBANs and support SEPA direct debit, reducing manual effort and payment failures for global SaaS companies.

The Bottom Line

The IBAN is the “passport” for your bank account. For businesses scaling internationally, mastering IBAN usage is the key to faster processing, lower rejection fees, and seamless global payment reconciliation.

Are you looking to automate the collection of IBANs for international customers, or are you troubleshooting a specific cross-border payment issue?

An IBAN (International Bank Account Number) is a standardized code of up to 34 alphanumeric characters that uniquely identifies a bank account for cross-border transfers. It’s the international banking system’s answer to a simple problem: how do you send money accurately when every country formats account numbers differently? This guide covers how IBANs are structured, where they’re used, how to find yours, and when businesses need them for international payments.

What Is an IBAN Number

What is an IBAN and why does it matter for international banking?

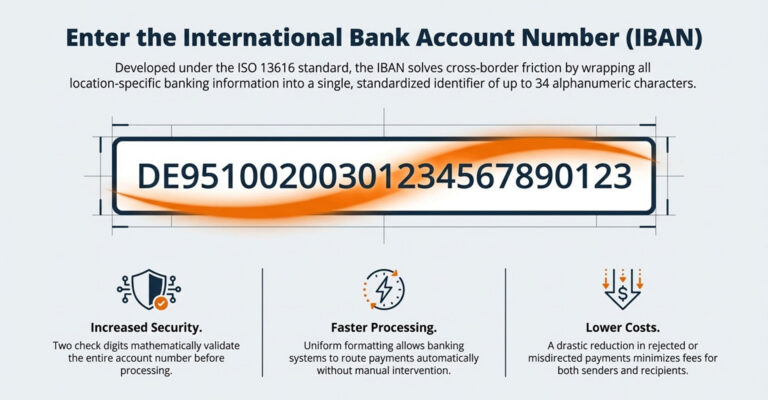

An International Bank Account Number (IBAN) is a standardized alphanumeric code of up to 34 characters that uniquely identifies a bank account for cross-border transfers. Developed under ISO 13616, the IBAN system enables secure, fast, and accurate international payments across Europe, the Middle East, and more than 65 other countries.

Before IBANs existed, international transfers relied on inconsistent domestic formats. A payment from Germany to France might include different account number lengths, varying bank codes, and no standardized way to verify accuracy. The result? Frequent errors, delays, and returned payments. The IBAN solves this by wrapping all the location-specific information banks require into a single, standardized identifier. Every IBAN contains a country code, check digits for validation, and the domestic account details—all in a predictable format that automated systems can process without manual intervention.

- Increased security: Two check digits mathematically validate the entire account number before processing.

- Faster processing: The uniform format allows banks to route payments automatically.

- Lower costs: Fewer rejected or misdirected payments mean reduced fees for both senders and recipients.

IBAN Structure and Format Explained

How is an IBAN code structured?

Every IBAN follows a consistent pattern with three core components, though the total length varies by country. Understanding this structure helps you verify that an IBAN is formatted correctly before initiating a transfer.

Country Code

The first two characters are always alphabetic letters representing the country where the account is held. DE indicates Germany, GB indicates the United Kingdom, FR indicates France, and so on. This tells the receiving bank which country’s banking system to route the payment through.

Check Digits

Immediately following the country code are two numeric digits calculated using a mathematical algorithm called MOD 97. If even one character in the IBAN is incorrect, the check digit calculation will fail. This catches typos and transcription errors before the payment is sent, rather than after it bounces back days later.

Basic Bank Account Number

The remaining characters form the BBAN (Basic Bank Account Number), which contains the domestic bank code, branch identifier, and account number. The BBAN’s length and internal structure vary by country based on local banking standards. Germany uses 18 characters for its BBAN, while the UK uses 14, and France uses 23.

IBAN Examples by Country

What does an IBAN look like in different countries?

The following examples illustrate how IBAN formats vary in length while maintaining the same structural principles.

| Country | Code | Length | Example Format |

|---|---|---|---|

| United Kingdom | GB | 22 | GB29 NWBK 6016 1331 9268 19 |

| Germany | DE | 22 | DE89 3704 0044 0532 0130 00 |

| France | FR | 27 | FR14 2004 1010 0505 0001 3M02 606 |

| Spain | ES | 24 | ES91 2100 0418 4502 0005 1332 |

| Netherlands | NL | 18 | NL91 ABNA 0417 1643 00 |

Spaces are added for readability when displaying IBANs, but the actual code is transmitted without spaces. The country code and check digits always appear first, followed by the country-specific BBAN.

How to Find Your IBAN Number

How do I find my IBAN number?

Locating your IBAN depends on your bank and country, but several reliable methods work across most institutions.

- Bank statements: Look for the IBAN printed near your account number on paper or electronic statements.

- Online banking portal: Log into your bank’s website and navigate to account details—the IBAN typically appears alongside your domestic account number.

- Mobile banking app: Check your account information or settings section.

- Contact your bank: Call customer service or visit a branch to request your IBAN directly.

- Debit card: If your bank is located in a country that uses IBANs, the number is often printed on your card.

Some banks and third-party websites offer IBAN calculator tools that generate an IBAN from your domestic account details. However, you’ll want to verify any calculated result with your bank before using it for a transfer.

IBAN vs SWIFT Code vs Routing Number

What is the difference between an IBAN, SWIFT code, and routing number?

These identifiers serve complementary but distinct purposes in banking, and understanding when to use each one prevents payment delays.

| Identifier | Purpose | Format | Primary Use |

|---|---|---|---|

| IBAN | Identifies specific bank account | Up to 34 alphanumeric | International transfers (Europe, Middle East) |

| SWIFT/BIC | Identifies the bank institution | 8 or 11 characters | Global bank-to-bank communication |

| Routing Number | Identifies US bank and branch | 9 digits | US domestic transfers (ACH, wire) |

IBAN vs SWIFT Code

An IBAN identifies the specific account receiving funds, while a SWIFT code (also called a BIC) identifies the bank itself. For many international transfers, you’ll provide both. The SWIFT code routes the payment to the correct bank, and the IBAN directs it to the correct account within that bank.

IBAN vs BIC Code

BIC stands for Bank Identifier Code, and it’s essentially the same thing as a SWIFT code. The terms are used interchangeably in international banking, so when a form asks for a BIC, you can provide the SWIFT code.

IBAN vs Routing Number

Routing numbers are specific to the United States and identify banks for domestic ACH and wire transfers. They serve a similar purpose to the bank code portion of an IBAN but are not interchangeable. US banks do not issue IBANs, so international transfers to the US use routing numbers combined with SWIFT codes instead.

IBAN vs Bank Account Number

Your domestic bank account number is actually embedded within your IBAN. The IBAN wraps your existing account details with a country code and check digits, creating a standardized format that works across international banking systems. Think of it as your account number dressed up for international travel.

Which Countries Use IBAN Numbers

Which countries require an IBAN for bank transfers?

The IBAN system originated in Europe and has since expanded to over 80 countries, though adoption is not universal.

- SEPA countries: All European Union member states plus Iceland, Liechtenstein, Norway, Switzerland, and Monaco use IBANs for euro transfers. SEPA (Single Euro Payments Area) mandates IBAN usage for cross-border payments within the zone.

- Middle East: Countries including the UAE, Saudi Arabia, Israel, and Turkey have adopted the IBAN standard.

- Caribbean and Africa: Partial adoption exists in countries like Mauritius, Tunisia, and several Caribbean nations.

- Non-IBAN countries: The United States, Canada, Australia, and New Zealand have not adopted the IBAN system. Transfers to these countries use SWIFT codes combined with domestic account details.

When sending money internationally, check whether the destination country uses IBANs. If it does, the recipient’s bank will require one.

How to Validate an IBAN Code

How can you verify an IBAN is correct before sending a payment?

Validation is worth the extra step. An incorrect IBAN can result in failed payments, returned transactions, or—in rare cases—funds sent to the wrong account entirely.

- Online IBAN validators: Third-party tools check the format, verify the check digits, and sometimes confirm the bank’s existence.

- Check digit calculation: The two check digits use a MOD 97 algorithm that validates the entire IBAN mathematically.

- Bank verification: Some banks validate IBANs before processing transfers and will flag errors during payment setup.

Always confirm the IBAN directly with the recipient rather than relying solely on automated validation. A valid IBAN format doesn’t guarantee it belongs to the intended recipient.

When Businesses Need an IBAN for International Payments

When do businesses need to collect or provide IBAN numbers?

Companies operating across borders encounter IBANs in several common scenarios, particularly when dealing with European customers or vendors.

- Paying international suppliers: Wire transfers to vendors in IBAN-using countries require the supplier’s IBAN for accurate routing.

- Collecting from global customers: Businesses accepting SEPA direct debit or international bank transfers from European customers collect IBANs during onboarding.

- Recurring billing across borders: Subscription and SaaS businesses billing European customers typically collect IBANs to enable automated payment collection via SEPA direct debit.

- Multi-currency invoicing: When accepting payments in local currencies, IBANs ensure accurate routing to the correct account.

For recurring revenue businesses, managing international payment details adds operational complexity. The more countries you bill, the more payment methods and account formats you’ll encounter.

Simplify Global Payment Collection for Recurring Revenue

Managing international payment details like IBANs adds complexity for subscription businesses, especially those scaling across multiple currencies and regions. Recurring billing platforms can automate multi-currency collection, support SEPA direct debit and global bank transfers (including US ACH, PAD, BACS, and SEPA), and reconcile payments automatically. This reduces manual effort, minimizes payment failures from incorrect account details, and keeps customer balances accurate across billing and accounting systems.

Frequently Asked Questions about IBANs

Do US banks issue IBAN numbers to account holders?

No. US banks do not issue IBANs because the United States has not adopted the IBAN system. For domestic transfers, US banks use routing numbers (9 digits) combined with account numbers. For international transfers, US banks use SWIFT codes. If someone requests your IBAN and you have a US bank account, provide your routing number, account number, and SWIFT code instead.

Can my IBAN change if I switch bank branches?

Generally no. Your IBAN is tied to your specific account and remains the same regardless of which branch you visit. However, opening a new account at a different bank would generate a new IBAN. Some banks may also issue new IBANs during mergers or system migrations, though this is uncommon.

What happens if I enter an incorrect IBAN on a payment?

The payment may be rejected, delayed, or potentially sent to the wrong account. The check digits help catch many errors before processing, but they cannot verify that the IBAN belongs to your intended recipient. If a payment goes to the wrong account, recovering the funds can be difficult and time-consuming. Always verify the IBAN directly with the recipient before initiating a transfer.

Is an IBAN required for all international wire transfers?

Not universally. An IBAN is required for transfers to countries that have adopted the standard, but transfers to non-IBAN countries like the US, Canada, or Australia use SWIFT codes combined with domestic account details. When in doubt, ask the recipient’s bank what information they require.

Do I need an IBAN for domestic bank transfers within my country?

It depends on your country. Many European countries now require IBANs even for domestic transfers, particularly within the SEPA zone. Countries like the US, Canada, and Australia use routing numbers or sort codes for internal payments and do not use IBANs domestically.