TL;DR: Canadian Pre-Authorized Debits (PAD)

Pre-authorized debit (PAD) is a secure payment method that allows Canadian businesses to “pull” funds directly from a customer’s bank account. Governed by Payments Canada’s Rule H1, it is the standard for reliable, high-volume recurring billing within Canada.

Key Takeaways

-

The Model: Unlike credit cards where the customer “pushes” payment, PAD allows the business to initiate withdrawals based on a signed agreement. Transactions settle through the ACSS network, typically within three to five business days.

-

Ideal Context: Highly effective for SaaS subscriptions, B2B invoices, and utility payments. It offers significantly lower fees than credit cards and reduces churn caused by expired or lost cards.

-

Implementation Steps:

-

Obtain Authorization: Secure a compliant PAD agreement (written, electronic, or verbal) before the first withdrawal.

-

Provide Notification: For variable amounts, you must notify the customer at least 10 days before the debit occurs.

-

Verify Banking Details: Collect the customer’s transit number, institution number, and account number.

-

Billing Tech: Use recurring billing platforms to automate the 10-day notices, retry failed transactions, and reconcile payments automatically.

-

The Bottom Line

PAD is the most cost-effective “set-and-forget” payment rail for the Canadian market. For businesses scaling internationally, mastering PAD—and distinguishing it from the US ACH system—is essential for maintaining predictable cash flow and a professional customer experience in Canada.

Are you looking to automate your Canadian PAD collection process, or do you need help drafting a Rule H1-compliant authorization agreement?

Pre-authorized debit (PAD) is a payment method that allows Canadian businesses to withdraw funds directly from a customer’s bank account after receiving written consent. Governed by Payments Canada’s Rule H1, PADs process through the Automated Clearing Settlement System and typically settle within three to five business days.

For recurring revenue businesses, PAD offers lower transaction costs than credit cards and more predictable cash flow than manual invoicing. This guide covers how PAD works, compliance requirements, setup steps, and how to handle failed transactions and disputes.

What Is a Pre-Authorized Debit Payment in Canada

What does pre-authorized debit mean and how does it work?

A pre-authorized debit (PAD) is a payment method that allows a business to withdraw funds directly from a customer’s bank account after receiving written consent. Governed by Payments Canada’s Rule H1, PADs require a signed authorization agreement before any transaction can occur. The payment processes through Canada’s Automated Clearing Settlement System (ACSS), and settlement typically takes three to five business days.

With credit card payments, the customer initiates the transaction. PAD flips that model—the business pulls funds on a scheduled basis. This makes PAD well-suited for recurring payments like subscriptions, utility bills, and loan repayments.

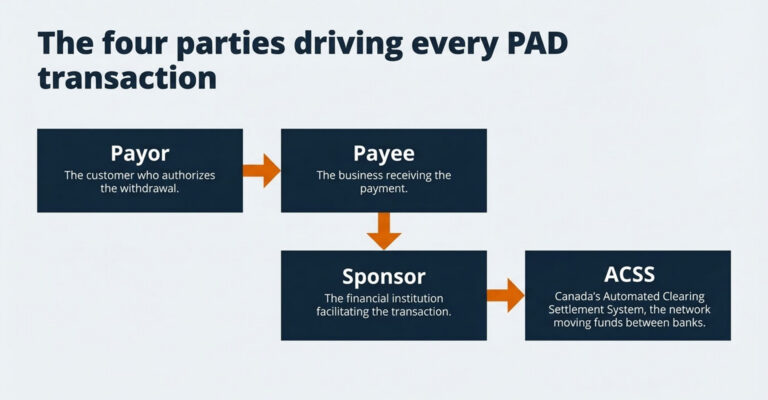

Four parties are involved in every PAD transaction:

- Payor: The customer who authorizes the withdrawal

- Payee: The business receiving the payment

- Sponsor: The financial institution facilitating the transaction

- ACSS: The clearing network that moves funds between banks

How Pre-Authorized Debits Work in Canada

How does the PAD payment process flow from authorization to settlement?

The PAD process starts with authorization and ends with funds arriving in the business’s account. Each step follows specific rules set by Payments Canada.

The PAD Authorization Process

Before withdrawing any funds, a business obtains explicit consent through a pre-authorized debit agreement. This authorization can be collected in writing, electronically, or verbally (though verbal consent has additional documentation requirements).

The agreement establishes the terms under which the business can debit the customer’s account. Once signed, the business retains this agreement as proof of authorization—a critical document if disputes arise later.

PAD Transaction Processing and Settlement

After authorization, the business submits payment requests to their sponsoring financial institution in batches. The sponsor forwards these requests through the ACSS network, which routes them to the payor’s bank.

Standard PAD transactions settle within three to five business days. Some processors offer faster settlement for an additional fee.

Types of Pre-Authorized Debit Categories

Payments Canada defines three PAD categories, each with different rules:

- Personal PADs: Consumer bill payments for utilities, subscriptions, and gym memberships

- Business PADs: B2B transactions between companies

- Cash Management PADs: Internal corporate fund transfers between accounts owned by the same entity

Benefits of Pre-Authorized Debits for Recurring Revenue Businesses

Why do SaaS and subscription businesses use PAD for payment collection?

For companies billing customers on a recurring basis, PAD offers advantages over credit cards and manual payment methods.

Lower Transaction Costs Than Credit Cards

PAD fees are typically flat rates rather than percentages. For a $500 monthly invoice, a credit card might cost $15 or more in processing fees at 3%, while PAD might cost $0.50 to $2.00 per transaction. This cost structure becomes more favorable as invoice amounts grow.

Improved Cash Flow Predictability

With PAD, businesses control when payments are collected rather than waiting for customers to initiate payment. Finance teams can schedule collections to align with their own payment obligations.

Reduced Involuntary Churn from Payment Failures

Credit cards expire, get lost, or hit spending limits. Bank accounts tend to remain stable for years. This stability translates to fewer failed payments for subscription businesses.

Simplified Reconciliation and Cash Application

PAD payments arrive with consistent reference data, making it easier to match incoming funds to outstanding invoices. Billing platforms like Ordway can automatically apply PAD receipts to customer accounts.

Pre-Authorized Debit Agreement Requirements

What elements are required in a valid PAD agreement?

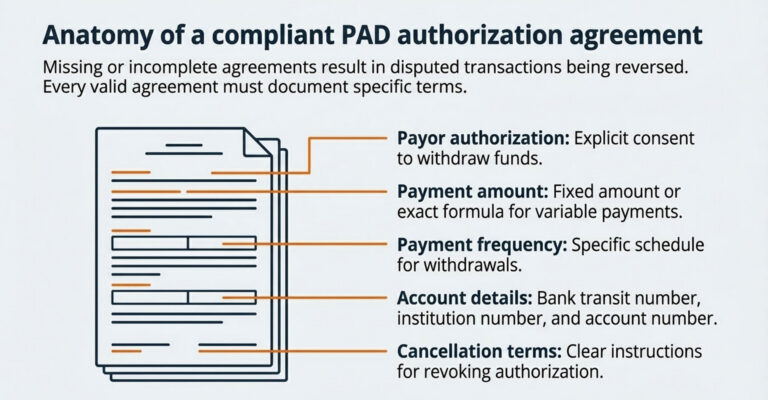

A compliant PAD agreement documents the terms of the payment arrangement. Missing or incomplete agreements can result in disputed transactions being reversed.

Required PAD Agreement Elements

Every PAD agreement includes specific information to be valid under Payments Canada rules:

- Payor authorization: Explicit consent to withdraw funds

- Payment amount: Fixed amount or formula for variable payments

- Payment frequency: Schedule for withdrawals (monthly, quarterly, etc.)

- Account details: Bank transit number, institution number, and account number

- Cancellation terms: Instructions for how the payor can revoke authorization

Written Confirmation and Notification Obligations

After obtaining authorization, businesses provide written confirmation of the agreement to the payor. For variable-amount PADs, the payee notifies the customer at least ten days before each withdrawal with the specific amount to be debited.

Record Retention and Documentation Standards

Businesses retain PAD agreement records for a minimum period after the last transaction. Organized documentation becomes essential when defending against unauthorized PAD claims.

Payments Canada Rule H1 Compliance

What regulatory requirements govern PAD processing in Canada?

Rule H1 is the regulatory framework governing all pre-authorized debit activity in Canada. Violations can result in transaction reversals, fines, and loss of PAD processing privileges.

Sponsor and Payment Service Provider Requirements

Businesses cannot process PADs directly through the ACSS network. Instead, they work through a sponsoring financial institution or a payment service provider with a sponsor relationship. The sponsor assumes responsibility for ensuring their clients comply with Rule H1.

Payor Notification and Consent Standards

Rule H1 specifies how consent is obtained and documented. Electronic authorizations are permitted but require the ability to produce a paper copy on demand. For variable amounts, the ten-day advance notification gives payors time to ensure sufficient funds are available.

How to Set Up Pre-Authorized Debit Collection

What steps does a business take to start accepting PAD payments?

Implementing PAD collection requires establishing relationships, creating compliant documentation, and configuring billing systems.

Step 1. Establish a Sponsor Relationship

Identify a financial institution or payment processor that can sponsor PAD transactions. Many payment gateways handle the sponsor relationship on your behalf.

Step 2. Create Compliant PAD Agreement Templates

Develop agreement templates that include all required elements under Rule H1. Many businesses embed PAD authorization into their service agreements or checkout flows.

Step 3. Collect and Verify Customer Banking Information

Gather the customer’s institution number, transit number, and account number. Verification methods include instant bank verification or traditional micro-deposits.

Step 4. Configure Payment Processing Workflows

Set up recurring payment schedules in your billing system and integrate with your payment processor. Platforms like Ordway automate this workflow from scheduling through cash application.

PAD Processing Timelines and Notification Requirements

How long does PAD processing take and when are customers notified?

For variable-amount PADs, businesses provide at least ten calendar days’ notice before withdrawing funds. This notification includes the specific amount to be debited.

Standard PAD transactions take three to five business days to settle after submission. During this window, the transaction can still be returned for insufficient funds or other reasons. PADs are not guaranteed payments.

Handling Dishonoured and Failed PAD Transactions

What happens when a PAD payment fails?

Unlike credit card declines that happen instantly, PAD failures may not surface for several days after submission.

Common failure reasons include:

- Insufficient funds: Account balance too low

- Account closed: Customer changed bank accounts

- Invalid account information: Incorrect bank details on file

- Payment stopped: Customer requested their bank block the transaction

When a PAD fails, the business receives a return notification from their processor. Automated retry logic can help recover some failed payments. For persistent failures, dunning workflows notify customers and request updated payment information. Ordway’s automated dunning handles these communications automatically.

PAD Disputes and Consumer Recourse

What recourse do customers have if they dispute a PAD transaction?

Customers can dispute PAD transactions through their financial institution within specific timeframes.

| PAD Type | With Valid Agreement | Without Valid Agreement |

|---|---|---|

| Personal PAD | 90 days | 90 days |

| Business PAD | 10 business days | 90 days |

When a customer disputes a PAD, the business produces the signed authorization agreement. Without proper documentation, the transaction will likely be reversed.

Pre-Authorized Debit vs Other Canadian Payment Methods

How does PAD compare to credit cards and other payment options?

Each payment method has trade-offs around cost, speed, and customer preference.

| Feature | PAD | Credit Card | Interac e-Transfer |

|---|---|---|---|

| Transaction cost | Flat fee ($0.50–$2) | Percentage (2–3%) | Flat fee ($1–$2) |

| Processing time | 3–5 business days | Instant | Minutes to hours |

| Best for | Recurring B2B invoices | Consumer transactions | One-time payments |

Canadian PAD vs US ACH

For businesses operating in both Canada and the United States, PAD and ACH are separate payment networks with different rules. A company cannot use US ACH credentials to collect Canadian payments. Each country requires its own setup, though most billing platforms support both networks through a single integration.

Automating PAD for Recurring Payment Collection

How can subscription businesses automate PAD workflows?

Manual PAD management—tracking authorizations, scheduling payments, handling failures, and reconciling receipts—becomes unsustainable as customer counts grow.

Modern billing platforms handle the entire PAD lifecycle: storing authorization agreements, scheduling recurring withdrawals, retrying failed transactions, sending dunning communications, and applying successful payments to customer accounts. Ordway’s Recurring Payments capabilities automate PAD alongside credit cards and US ACH, providing a unified view of payment status across all collection methods.

Frequently Asked Questions

Can pre-authorized debit be used for variable or usage-based billing amounts?

Yes, PAD supports variable amounts. Businesses notify the payor at least ten days before each withdrawal with the specific amount to be debited.

How does Canadian PAD differ from US ACH for cross-border businesses?

PAD and ACH are separate payment networks governed by different rules. Businesses operating in both countries set up distinct configurations for each.

Which payment gateways support Canadian pre-authorized debit processing?

Major gateways including Stripe, GoCardless, and Plooto support Canadian PAD. Verify PAD capabilities specifically when evaluating processors.

How long does it take to receive funds from a Canadian PAD transaction?

Standard PAD settlement takes three to five business days from submission.

What happens if a customer closes their bank account after signing a PAD agreement?

The PAD transaction will be returned as dishonoured. The business then contacts the customer to obtain updated banking information or arrange an alternative payment method.