CHAPS is the UK’s same-day payment system for high-value sterling transfers, operated by the Bank of England with guaranteed settlement and no upper limit on transaction amounts. Whether you’re completing a property purchase, making a large supplier payment, or meeting a tax deadline, CHAPS ensures funds arrive the same business day—irrevocably.

This guide covers how CHAPS works, what it costs, how it compares to Bacs and Faster Payments, and when it makes sense to use it over other UK payment methods.

What is a CHAPS payment

What is a CHAPS payment and why do businesses use it?

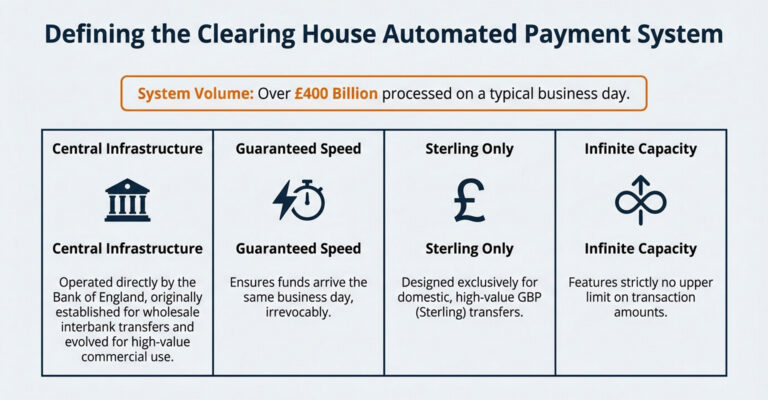

CHAPS is a UK-based, same-day, high-value electronic payment system operated by the Bank of England. It guarantees secure, irrevocable sterling transfers with no upper limit on the amount you can send—making it the go-to method for property purchases, large corporate transactions, and time-sensitive tax payments.

Unlike standard bank transfers that may take hours or even days to clear, CHAPS ensures funds arrive the same business day. The system processes over £400 billion in transactions on a typical business day, which makes it one of the largest payment systems in the world by value.

What does CHAPS stand for

CHAPS stands for Clearing House Automated Payment System. Originally established to handle wholesale interbank transfers between financial institutions, the system has since evolved to serve both business and personal high-value payments.

How CHAPS differs from regular bank transfers

While both CHAPS and regular bank transfers move money between accounts, a few key distinctions set them apart:

- Settlement speed: CHAPS settles same-day with guaranteed finality, whereas standard transfers may take longer depending on the method

- Finality: Once processed, CHAPS payments cannot be recalled or reversed

- Fee structure: CHAPS typically carries a flat transaction fee; regular transfers are often free

- Payment limits: CHAPS has no maximum transfer amount, while other methods may impose caps

How the CHAPS payment system works

How does the CHAPS payment system process transactions?

CHAPS operates through the Bank of England’s Real-Time Gross Settlement (RTGS) infrastructure. Each payment instruction flows from the sender’s bank to the recipient’s bank, settling individually and immediately in central bank money.

When you initiate a CHAPS transfer, your bank submits the payment instruction to the RTGS system. The Bank of England then debits your bank’s settlement account and credits the recipient’s bank in real time. There’s no batching or netting involved—each payment settles on its own.

Real-time gross settlement explained

Real-Time Gross Settlement (RTGS) means each payment is processed and settled individually the moment it’s submitted. This differs from batch systems like Bacs, which accumulate payments throughout the day and settle them together.

The “gross” in RTGS indicates that payments settle at their full value rather than being netted against other transactions. This approach eliminates settlement risk—once a CHAPS payment is confirmed, the funds are guaranteed.

CHAPS payment cut-off times

Banks typically set internal cut-off times for CHAPS submissions, often between 2:00 PM and 5:00 PM on business days. The CHAPS system itself operates from 6:00 AM to 6:00 PM UK time, Monday through Friday, excluding bank holidays.

If you submit a CHAPS request after your bank’s cut-off, the payment will be processed the next business day. Cut-off times vary by institution and account type, so checking with your specific bank is worthwhile.

How long does a CHAPS payment take

How long does a CHAPS payment take to arrive?

CHAPS payments typically arrive the same business day, often within a few hours of submission. The exact timing depends on when you initiate the transfer relative to your bank’s cut-off time.

For payments submitted early in the day, funds usually reach the recipient’s account within two to three hours. Payments submitted closer to the cut-off may arrive later in the afternoon but will still settle before the end of the business day.

How much does a CHAPS payment cost

What fees apply when you pay by CHAPS?

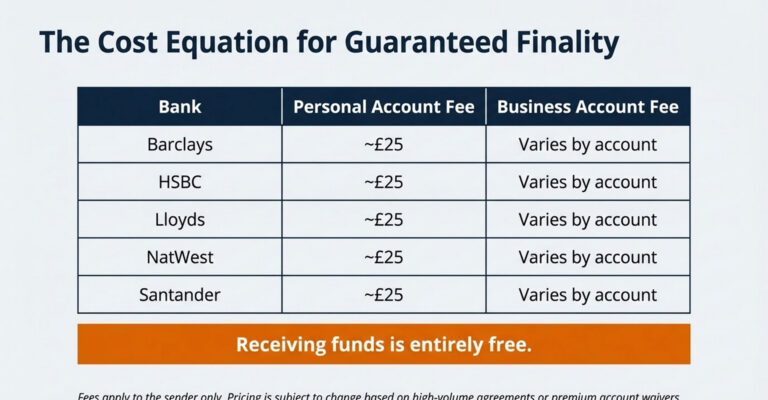

Banks charge a flat fee per CHAPS transfer, typically ranging from £20 to £35 for personal accounts. Business accounts may have different fee structures, sometimes with lower per-transaction costs for high-volume users.

Receiving a CHAPS payment is generally free—the fee applies only to the sender. Some banks waive CHAPS fees for premium account holders or include a certain number of free transfers per month.

CHAPS Payment Limits and Minimums

Is there a minimum or maximum amount for CHAPS payments?

CHAPS has no upper limit on transfer amounts, which is precisely why it’s the method of choice for high-value transactions like property completions and large corporate payments.

While there’s technically no minimum either, the transaction fee makes CHAPS impractical for small amounts. Most people use CHAPS when the payment value justifies the cost—typically for transactions above £10,000, though the threshold depends on urgency and individual circumstances.

How to make a CHAPS payment

How do you make a CHAPS transfer?

You can initiate a CHAPS payment through your bank via online banking (if supported), telephone banking, or by visiting a branch in person. The process is straightforward, though it requires gathering specific information beforehand.

1)Gather the required payment details

Before initiating your transfer, you’ll want to have the following on hand:

- Recipient’s full name (as it appears on their bank account)

- Recipient’s sort code (six digits)

- Recipient’s account number (eight digits)

- Payment amount in GBP

- Payment reference (for identification purposes)

Double-check all details carefully—CHAPS payments cannot be reversed once processed.

2) Submit your CHAPS transfer request

Contact your bank through your preferred channel to request the CHAPS transfer. Some banks offer CHAPS through online banking, while others require a phone call or branch visit.

You’ll provide all the payment details and confirm the transaction. Most banks will ask you to verify your identity before processing high-value payments.

3) Confirm same-day settlement

Your bank will provide confirmation once the payment has been submitted to the CHAPS system. Keep this confirmation for your records—it serves as proof of payment and helps with reconciliation.

The recipient’s bank will credit the funds to their account, typically the same day. You can contact your bank directly if you want a status update on the transfer.

What CHAPS payments are used for

When is CHAPS the right choice?

CHAPS is ideal whenever same-day settlement and payment finality are essential. The combination of speed, certainty, and unlimited transfer amounts makes it suitable for specific high-stakes scenarios.

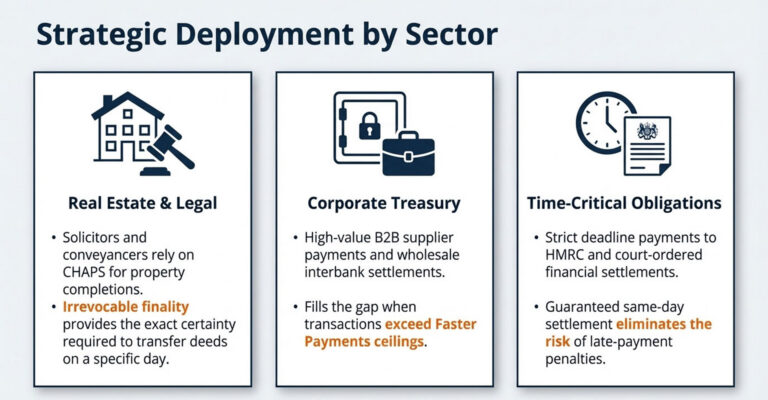

Property transactions and conveyancing

Solicitors and conveyancers rely on CHAPS for property completions, where funds must arrive on a specific day and time. The irrevocable nature of CHAPS provides the certainty required for legal transactions—once the payment is confirmed, the sale can proceed.

High-value B2B and wholesale payments

Businesses use CHAPS for large supplier payments, intercompany transfers, and treasury operations. When a payment is too large for Faster Payments limits or too urgent for Bacs, CHAPS fills the gap.

Time-critical tax and legal payments

CHAPS is commonly used for HMRC payments with strict deadlines, court-ordered payments, and other time-sensitive obligations. When late payment carries penalties or legal consequences, the guaranteed same-day settlement of CHAPS provides certainty.

Which UK banks use CHAPS

Which banks participate in the CHAPS payment system?

All major UK banks and building societies offer CHAPS services to their customers. However, not all banks connect to the system in the same way.

Direct participants connect directly to the Bank of England’s RTGS infrastructure and can submit payments themselves. Indirect participants access CHAPS through a direct participant, which processes payments on their behalf. The Bank of England maintains the official list of CHAPS participants on its website.

Are CHAPS payments secure

Is a CHAPS transfer secure?

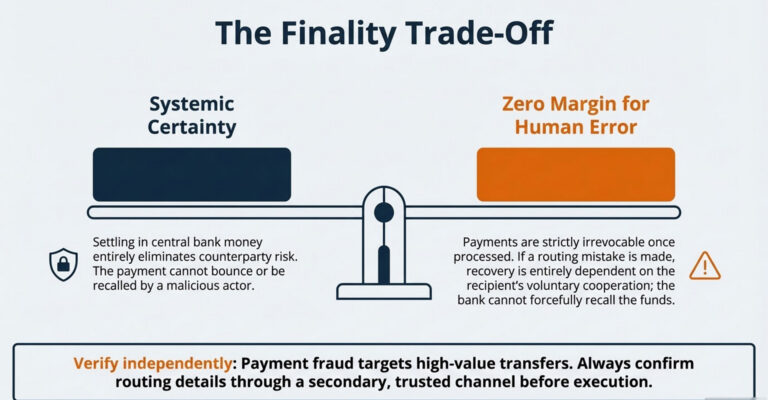

CHAPS is one of the most secure payment methods available in the UK. Operated by the Bank of England with robust security controls, it settles in central bank money, which eliminates counterparty risk entirely.

That said, security also depends on the user. Since CHAPS payments are irrevocable, verifying recipient details carefully before submitting is essential. Payment fraud often targets high-value transfers, so confirming bank details through a trusted channel is a good practice.

CHAPS vs Bacs payments

What is the difference between Bacs and CHAPS?

Both are UK payment systems, but they serve different purposes and operate on different timelines. Understanding when to use each can save you money and ensure your payments arrive when expected.

| Feature | CHAPS | Bacs |

|---|---|---|

| Settlement | Same-day | Three working days |

| Cost | £20–£35 per transaction | Typically free or low cost |

| Limits | No upper limit | Varies by bank |

| Best for | Urgent, high-value payments | Recurring, routine payments |

Settlement speed

CHAPS settles on the same business day, while Bacs operates on a three-day cycle. If you submit a Bacs payment on Monday, the recipient typically receives funds on Thursday.

Transaction fees

CHAPS charges a fee per payment, whereas Bacs is typically free or very low cost for regular payments. For routine transactions where timing isn’t critical, Bacs offers significant cost savings.

Payment limits

CHAPS has no practical upper limit, making it suitable for transactions of any size. Bacs may have limits depending on the bank, though limits are generally sufficient for payroll and regular supplier payments.

- CHAPS: Property purchases, urgent supplier payments, tax deadlines, large one-off transfers

- Bacs: Payroll, Direct Debits, regular supplier payments, standing orders, subscription billing

Can a CHAPS payment be reversed

Can you reverse or cancel a CHAPS payment?

No—CHAPS payments are final and irrevocable once processed. This finality is actually a feature, not a limitation; it’s what makes CHAPS suitable for high-value transactions where both parties want certainty.

If you make an error, contact your bank immediately. Recovery depends entirely on the recipient’s cooperation, as your bank cannot simply recall the funds. This is why verifying all details before submitting is so important.

Who uses CHAPS payments

Who typically uses CHAPS transfers?

The system serves a range of users with different payment requirements:

- Solicitors and conveyancers: For property transaction completions

- Corporate treasury teams: For large intercompany and supplier payments

- Financial institutions: For wholesale and interbank settlements

- Businesses: For time-critical vendor payments and tax obligations

- Individuals: For house purchases and other high-value personal transactions

Benefits of CHAPS for business payments

Why do businesses choose CHAPS for GBP payments?

For companies making high-value or time-sensitive payments, CHAPS offers several advantages:

- Same-day finality: Funds arrive and settle the same business day

- No payment ceiling: Suitable for transactions of any size

- Certainty and reliability: Operated by the Bank of England with guaranteed settlement

- Audit trail: Clear confirmation and records for financial reconciliation

Streamlining GBP payment reconciliation for recurring revenue businesses

How can subscription businesses manage high-value GBP payments efficiently?

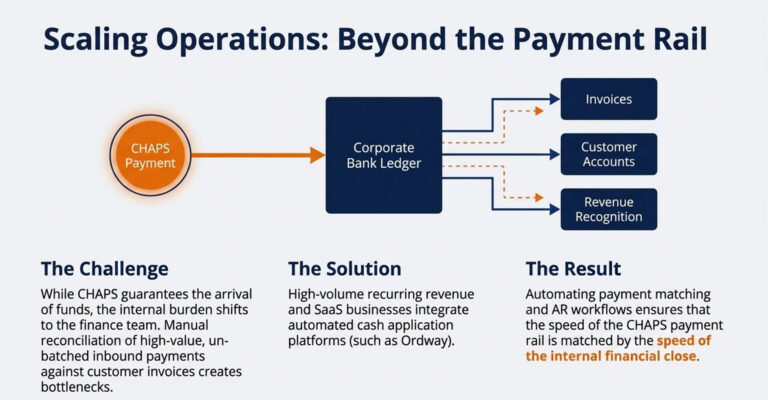

Companies receiving CHAPS payments from UK customers often face challenges reconciling incoming funds against invoices and customer accounts. Manual matching becomes increasingly difficult as payment volumes grow.

For recurring revenue businesses, automating cash application reduces reconciliation effort and accelerates the financial close. Billing platforms like Ordway help SaaS and subscription companies automate payment matching, AR workflows, and revenue recognition across multiple payment methods and currencies—including bank transfers like CHAPS.

Frequently Asked Questions about CHAPS UK Payments

What happens if a CHAPS payment fails?

If a CHAPS payment cannot be processed due to incorrect details, the sending bank will return the funds to your account. Contact your bank immediately to resolve the issue and resubmit with corrected information.

Can you make a CHAPS payment on weekends or bank holidays?

CHAPS only operates on UK business days. Payments requested on weekends or bank holidays will be queued and processed the next working day.

Is CHAPS the same as SWIFT?

No—CHAPS is a domestic UK payment system for GBP transfers, while SWIFT is a global messaging network used for international payments. They serve different purposes and operate independently.

Are CHAPS payments limited to GBP only?

Yes, CHAPS processes only sterling (GBP) transactions. For payments in other currencies, you’ll want to use international transfer methods or foreign exchange services.

Do you need a UK bank account to receive a CHAPS payment?

Yes, the recipient requires a UK bank account with a valid sort code and account number to receive a CHAPS transfer.

How do you track a CHAPS transfer after sending?

Your bank provides a payment confirmation or reference number when you submit the transfer. Contact your bank directly for status updates if you want to track the payment.