Contract Assets in Revenue Recognition

A contract asset is an entity’s right to payment for goods or services already transferred to a customer, where that right depends on something other than the passage of time—such as completing another deliverable or reaching a project milestone. Under ASC 606 and IFRS 15, contract assets represent the gap between when revenue is recognized and when an unconditional right to bill exists.

This guide covers how to recognize, record, and present contract assets on your financial statements, along with the key differences between contract assets, receivables, and contract liabilities.

This guide covers how to recognize, record, and present contract assets on your financial statements, along with the key differences between contract assets, receivables, and contract liabilities.

What Is a Contract Asset

What is a contract asset and why does it matter for revenue recognition?

A contract asset is an entity’s right to consideration in exchange for goods or services that have been transferred to a customer, where that right is conditional on factors other than just the passage of time. Under ASC 606 and IFRS 15, contract assets arise when revenue is recognized before an unconditional right to payment exists.

You might hear contract assets called “unbilled revenue,” though the two terms aren’t always interchangeable. The key distinction is conditionality. A contract asset exists because something beyond waiting for a due date still stands between you and payment, such as completing another deliverable or hitting a project milestone.

- Conditional right: Payment depends on completing additional performance obligations, not simply waiting for the invoice date.

- Revenue timing mismatch: When revenue recognition outpaces billing, a contract asset appears on the balance sheet.

- Common industries: SaaS companies with bundled services, construction firms using percentage-of-completion, and professional services organizations frequently encounter contract assets.

When to Record a Contract Asset

When does your finance team recognize a contract asset on the balance sheet?

A contract asset is recorded under ASC 606 when an entity has satisfied a performance obligation and recognized revenue, but the right to payment remains conditional on something other than the passage of time.

Revenue Recognized Before Invoicing

This scenario occurs when goods or services have been transferred to the customer, but a billing milestone hasn’t yet been reached. For example, a SaaS company might deliver software but can only issue an invoice after customer training is complete. The revenue from the software delivery is recognized, but since the company can’t yet bill, a contract asset is recorded.

Performance Obligations Satisfied Over Time

In percentage-of-completion scenarios, a contract asset is recorded when the amount of revenue recognized exceeds the amounts billed to the customer. This is common in construction or for multi-phase SaaS implementations where work progresses faster than contractual billing milestones allow.

Reclassification to Accounts Receivable

A contract asset converts to an accounts receivable once the right to payment becomes unconditional. At that point, only the passage of time is required before payment is due. This reclassification is the fundamental distinction between the two asset types and typically happens when the final performance condition is satisfied.

How to Record Contract Assets Under ASC 606

How do finance teams record contract assets in compliance with ASC 606?

Recording contract assets involves specific journal entries that reflect the timing difference between revenue recognition and billing.

Recording Initial Contract Asset Recognition

To record the initial recognition of a contract asset:

- Debit: Contract Asset

- Credit: Revenue

For example, suppose a SaaS company delivers a software license worth $50,000 but cannot bill until pending training is complete. The company would record a $50,000 contract asset alongside the revenue. The asset sits on the balance sheet until the billing condition is met.

Reclassifying Contract Assets to Receivables

When the remaining conditions are satisfied and the right to payment becomes unconditional:

- Debit: Accounts Receivable

- Credit: Contract Asset

This entry simply moves the balance from one asset account to another. No income statement impact occurs at this stage because the revenue was already recognized when the contract asset was created.

Adjusting for Contract Modifications

Changes to contract terms, such as scope or price adjustments, require a reassessment of the contract. This may lead to an adjustment of the contract asset balance to reflect the modified transaction price or revised performance obligations. The accounting treatment depends on whether the modification is treated as a separate contract or as a change to the existing one.

Contract Asset vs Receivable

What is the difference between a contract asset and a receivable?

The core distinction is whether the right to payment is conditional or unconditional. A contract asset represents a conditional right to payment that depends on future performance, while an accounts receivable represents an unconditional right to payment that depends only on the passage of time.

| Characteristic | Contract Asset | Accounts Receivable |

|---|---|---|

| Right to payment | Conditional (depends on future performance) | Unconditional (only time passes) |

| Trigger | Revenue recognized before billing rights | Invoice issued or billing milestone reached |

| Balance sheet classification | Current asset (typically) | Current asset |

| Credit loss testing | Required under ASC 326 | Required under ASC 326 |

Think of it this way: if you’ve done the work and just wait for the due date, that’s a receivable. If you’ve done some work but still owe the customer something else before you can demand payment, that’s a contract asset.

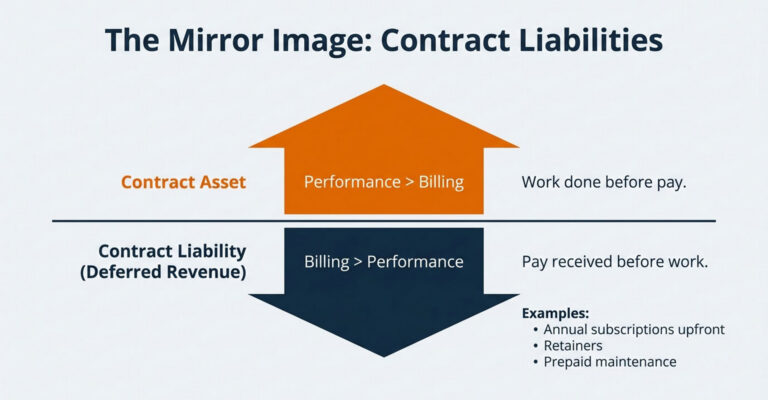

What Is a Contract Liability

What is a contract liability and how does it relate to contract assets?

A contract liability, often called deferred revenue, is an entity’s obligation to transfer goods or services to a customer for which the entity has already received consideration. Contract liabilities have an inverse relationship with contract assets: a contract asset arises when performance exceeds billing, while a contract liability arises when billing exceeds performance.

Examples include:

- Annual subscription paid upfront: A customer pays $120,000 for 12 months of service. The company recognizes $10,000 in revenue each month, and the remaining balance is a contract liability.

- Retainer or deposit: An advance payment received before services begin is recorded as a contract liability.

- Prepaid maintenance contracts: Payment collected before the support period starts creates a contract liability.

Contract Asset Examples

What are common contract asset scenarios in practice?

The following examples illustrate how contract assets and liabilities are recognized in different situations.

Contract Asset from Multiple Performance Obligations

Consider a SaaS contract worth $100,000, with $60,000 allocated to the software license and $40,000 to implementation services. The invoice is only due upon project completion.

When the software is delivered, the company recognizes $60,000 in revenue and records a corresponding $60,000 contract asset. This asset remains on the balance sheet until the implementation is complete and the right to payment becomes unconditional. At that point, the contract asset is reclassified to accounts receivable.

Contract Liability from Advance Payment

As a counterexample, if a customer pays $50,000 upfront for a 12-month subscription, the company records a $50,000 contract liability. This liability is reduced each month as revenue is earned, which is the opposite pattern from a contract asset.

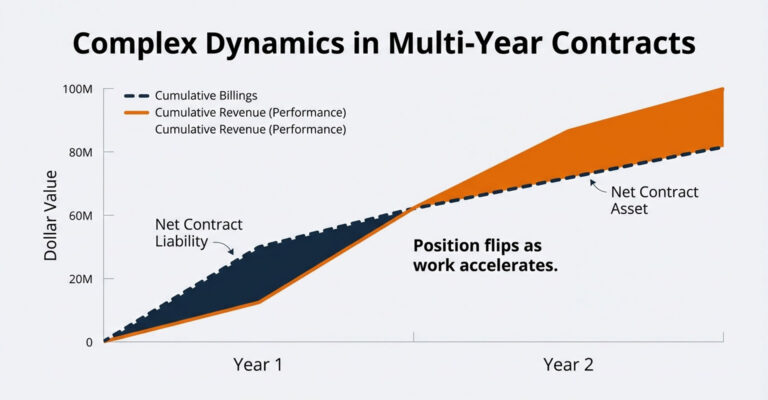

Multi-Year Contract with Bundled Services

A complex contract can shift between a contract asset and a liability over time. A customer’s Year 1 payment might exceed the value of performance delivered in Year 1, creating a contract liability. However, by Year 2, cumulative performance may catch up and exceed cumulative billings, causing the net position to shift to a contract asset.

How to Test Contract Assets for Impairment

Are contract assets subject to impairment testing?

Yes, contract assets are tested for credit losses under ASC 326 (CECL), similar to accounts receivable. Most nonbanks have financial instruments including contract assets that are subject to the CECL model. This testing is necessary because there’s a risk the customer may not pay even after all performance conditions are met.

Factors to consider include:

- Customer creditworthiness: Historical payment behavior and financial health

- Contract-specific risks: Complexity of remaining obligations and likelihood of disputes. Contract assets may take longer to recover than trade receivables since collection depends on factors beyond just the passage of time.

- Economic conditions: Industry trends and macroeconomic factors affecting the customer’s ability to pay

How to Present Contract Assets on Financial Statements

Where do contract assets appear on the balance sheet and what disclosures are required?

Proper presentation and disclosure are critical for compliance with accounting standards.

Balance Sheet Presentation

Contract assets are classified as current or non-current based on when they’re expected to be reclassified to receivables. For a single contract, any contract assets and contract liabilities are presented on a net basis. The line item on the balance sheet may be labeled “Contract asset,” “Unbilled revenue,” or a similar term depending on company preference.

Required Disclosures Under ASC 606 and IFRS 15

Key disclosure requirements include:

- Opening and closing balances: A reconciliation of the opening and closing balances of contract assets and contract liabilities

- Revenue recognized: The amount of revenue recognized in the period that was included in the contract liability balance at the beginning of the period

- Significant judgments: Explanations of significant judgments made in applying the revenue standard

- Impairment losses: Any credit losses recognized on contract assets during the period

How to Automate Contract Asset Tracking

How can finance teams reduce manual effort in tracking contract assets?

Spreadsheet-based tracking is prone to errors and inefficiencies, especially as contract volume grows. Automation streamlines the process and enhances accuracy.

Integrate Billing and Revenue Recognition Systems

Connecting your CRM, billing platform, and general ledger eliminates manual data transfers and reduces errors. Modern platforms can extract contract data automatically to generate revenue schedules and the corresponding accounting entries without manual intervention.

Establish Automated Revenue Schedules

Automated systems calculate recognized versus deferred revenue amounts based on the rules for satisfying performance obligations. This triggers the correct contract asset and liability journal entries as performance occurs and billing milestones are reached.

Generate Audit-Ready Reports

Automated systems maintain a complete, auditable trail of all transactions and calculations, supporting ASC 606/IFRS 15 compliance and reducing audit risk. These systems can produce reconciliations and disclosure schedules automatically, which saves significant time during the close process.

Automate Contract Asset Management with Ordway

Ordway’s Revenue Recognition software automates contract asset tracking, revenue schedule generation, and compliance reporting under ASC 606/IFRS 15. By integrating with your billing and GL systems, Ordway provides a seamless solution for managing complex revenue streams.

Frequently Asked Questions

What is a contract asset example?

A SaaS company delivers software worth $60,000 but cannot bill until customer training is complete. The company recognizes $60,000 in revenue and records a contract asset because the right to payment depends on completing the training, not just waiting for a due date.

What is the difference between a contract asset and a receivable?

A contract asset represents a conditional right to payment that depends on future performance, while an accounts receivable represents an unconditional right where only time passes before payment is due. The contract asset converts to a receivable once all performance conditions are satisfied.

Is a contract asset a tangible asset?

No, a contract asset is an intangible asset that represents a conditional right to receive payment, not a physical item. Contract assets appear on the balance sheet as current or non-current assets depending on when the conditions are expected to be satisfied.

When to record a contract asset?

A contract asset is recorded when an entity satisfies a performance obligation and recognizes revenue, but the right to payment remains conditional on something other than the passage of time. This occurs when the value of work performed exceeds the amount the company can currently bill to the customer.

What is the difference between unbilled revenue and a contract asset?

These terms are often used interchangeably in practice. However, under ASC 606, “contract asset” is the specific technical term for unbilled amounts where the right to payment is conditional on future performance, not just the passage of time or an administrative task like sending an invoice.