TL;DR: Check Payments

A check payment is a written order directing a bank to pay a specific amount from the payer’s account to a named recipient. Despite the rise of digital alternatives, it remains a “workhorse” for B2B transactions, particularly in industries like construction, healthcare, and government.

Key Takeaways

-

The Model: Check payments operate on a multi-day cycle (typically 2–5 business days) involving issuance, deposit, interbank clearing, and final settlement.

-

Ideal Context: Best suited for high-value B2B transactions where a physical paper trail is valued, or for vendors who do not accept credit cards to avoid processing fees.

-

The Lifecycle: 1. Issuance: Payer completes the check; 2. Presentment: Recipient deposits the check via bank/app; 3. Clearing: Banks verify funds and settle the transfer; 4. Availability: Funds become accessible after any bank-imposed holds.

-

Risk Profile: Businesses must manage risks like Non-Sufficient Funds (NSF), check fraud (63% of businesses experienced this in 2024), and “stale-dated” checks (older than 6 months).

Implementation Steps

-

Verify Authenticity: Inspect large checks for security features like watermarks and confirm the written and numerical amounts match exactly.

-

Establish Clear Policies: Document accepted payment methods and specific fees for returned (bounced) checks in your contracts.

-

Automate Reconciliation: Use AR platforms to match check images or lockbox data to open invoices, reducing manual data entry and “days sales outstanding” (DSO).

-

Implement Internal Controls: Segregate duties so the person receiving the mail is not the same person depositing the checks to prevent internal fraud.

The Bottom Line

Check payments offer a reliable paper trail and zero recipient processing fees, but they carry a high administrative burden and slower clearing times. For scaling businesses, the goal is to automate check processing while gradually incentivizing customers to move toward lower-risk electronic rails like ACH.

Are you looking to set up a lockbox service to handle physical checks, or are you interested in how to transition your current check-paying customers over to ACH?

Check Payments

A check payment is a written order directing a bank to pay a specific amount from the payer’s account to a named recipient—a payment method that remains surprisingly common in B2B transactions despite the rise of digital alternatives.

This guide covers how check payments work from issuance through clearing, the different types of checks businesses encounter, the advantages and risks of accepting them, and practical strategies for managing check-based receivables efficiently.

What is a Check Payment?

What is a check payment and why does it still matter in business transactions?

A check payment is a written order that tells a bank to pay a specific amount of money from the payer’s account to a named recipient. When you write a check, you’re authorizing your bank to transfer funds on your behalf. The recipient deposits the check, their bank presents it to your bank, and the money moves between accounts—typically clearing within two to three business days.

In British English and Commonwealth countries, this same instrument is called a “cheque payable,” though the mechanics work identically. Despite the rise of digital payments, checks remain common in B2B transactions (25% of B2B payments), particularly in construction, healthcare, and government contracting where paper documentation still holds value.

Every check contains several elements that make it valid:

- Date: When the check is written, which affects when it can be deposited

- Pay to the order of: The recipient’s name (the payee)

- Numerical amount: The dollar figure in the small box

- Written amount: The same amount spelled out in words, which takes precedence if the two don’t match

- Memo line: An optional description of what the payment covers

- Signature: The account holder’s authorization

How Check Payments Work

How does a check payment move from the payer to the recipient’s account?

The journey from issuance to cleared funds involves multiple steps and typically takes two to five business days. Understanding this process helps explain why checks remain useful in some contexts—and why they create challenges in others.

1. Check Issuance

The payer fills out all required fields, ensuring the numerical and written amounts match exactly. The completed check is then delivered to the recipient through mail, in person, or as a scanned image. Accuracy matters here—discrepancies between numbers and words can cause the bank to reject the check or delay processing.

2. Deposit and Presentment

Once the recipient receives the check, they deposit it through a bank branch, ATM, or mobile deposit app. The recipient’s bank then “presents” the check to the payer’s bank, essentially requesting payment. This presentment happens through interbank clearing networks, often facilitated by the Federal Reserve.

3. Clearing and Settlement

During clearing, the payer’s bank verifies the account has sufficient funds and authorizes the transfer. Many banks now convert paper checks to electronic ACH transactions during this step, which speeds up processing. The actual settlement—when money moves between banks—typically happens within one to two business days after presentment.

4. Funds Availability

Even after a check clears, banks may place holds on the funds, particularly for large amounts, new accounts, or out-of-state checks. Regulation CC governs how long banks can hold deposited funds, but recipients often wait several days before the full amount becomes available.

Types of Check Payments

What are the different types of check payments used in business?

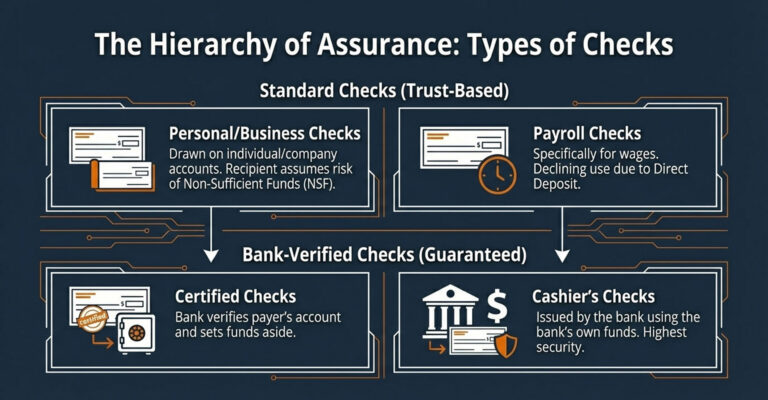

Not all checks carry the same level of assurance. The type determines who issues it, whether funds are guaranteed, and when it’s appropriate to use.

Personal Checks

Personal checks are drawn on an individual’s checking account and carry no bank guarantee. They’re commonly used for rent, services, or person-to-person payments. The recipient assumes the risk that funds may not be available.

Business Checks

Business checks are issued from a company’s account and typically include the company name and address. Some organizations require multiple signatures for amounts above a certain threshold. They function similarly to personal checks but provide clearer documentation for accounting purposes.

Certified Checks

A certified check is a personal or business check that the bank has verified and set aside funds for. This verification gives the recipient more confidence that the check won’t bounce, though it’s not quite as secure as a cashier’s check.

Cashier’s Checks

Cashier’s checks are issued directly by the bank using the bank’s own funds. Because the bank guarantees payment, these are often required for large transactions like real estate closings or vehicle purchases.

Payroll Checks

Payroll checks are business checks specifically issued for employee wages. While direct deposit has largely replaced them, some employers still use payroll checks, particularly for employees without bank accounts.

| Check Type | Issued By | Funds Guaranteed? | Common Use Case |

|---|---|---|---|

| Personal | Individual | No | Rent, services |

| Business | Company | No | Vendor payments, invoices |

| Certified | Bank-verified | Yes (set aside) | Large purchases |

| Cashier's | Bank | Yes | Real estate, vehicle purchases |

| Payroll | Employer | No | Employee wages |

Advantages of Check Payments

Why do businesses still accept check payments?

Even with electronic alternatives widely available, checks offer distinct benefits that keep them relevant in certain business contexts.

Paper Trail and Documentation

Checks create a physical or scanned record that includes the payee, amount, date, and payer’s signature. This documentation proves useful during audits, disputes, or when reconstructing payment history.

No Processing Fees for Recipients

Unlike credit card payments that carry interchange fees, depositing a check typically costs the recipient nothing. For businesses with thin margins or high-value transactions, avoiding processing fees can meaningfully impact profitability.

Wide Acceptance in B2B Transactions

Many industries—construction, healthcare, government, and professional services—still prefer or require checks. Some vendors don’t accept credit cards at all, and others charge convenience fees for electronic payments.

Payment Timing Control

Checks give both parties flexibility around timing. Payers can mail checks strategically to manage cash flow, while recipients can hold checks before depositing if needed.

Disadvantages of Check Payments

What are the drawbacks of relying on check payments?

Despite their benefits, checks create operational challenges that increasingly push businesses toward electronic alternatives.

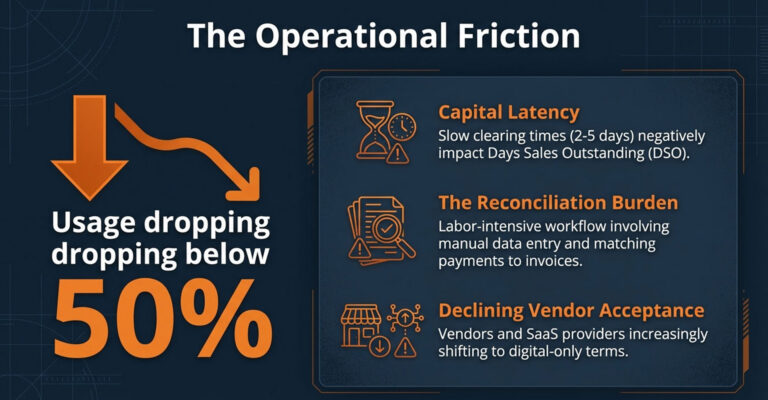

Slow Clearing Times

The multi-day clearing process delays cash availability compared to same-day or next-day electronic payments. For businesses tracking days sales outstanding (DSO), check payments extend collection timelines and complicate cash flow forecasting.

Manual Processing and Reconciliation Burden

Finance teams receiving checks face a labor-intensive workflow: opening mail, recording payment details, matching payments to invoices, preparing deposits, and reconciling accounts.

Fraud and Bounced Check Exposure

Checks can be forged, altered, or written on accounts with insufficient funds. The recipient bears the risk until the check fully clears—and even then, some fraudulent checks can be reversed weeks later.

Declining Acceptance Among Vendors

Some vendors and SaaS providers no longer accept checks, with check usage dropping below 50% among midsize businesses in 2025, pushing them toward electronic payment methods.

Risks of Accepting Check Payments

What risks do businesses face when accepting checks?

Beyond general disadvantages, specific risk categories warrant attention from finance teams evaluating their payment acceptance policies.

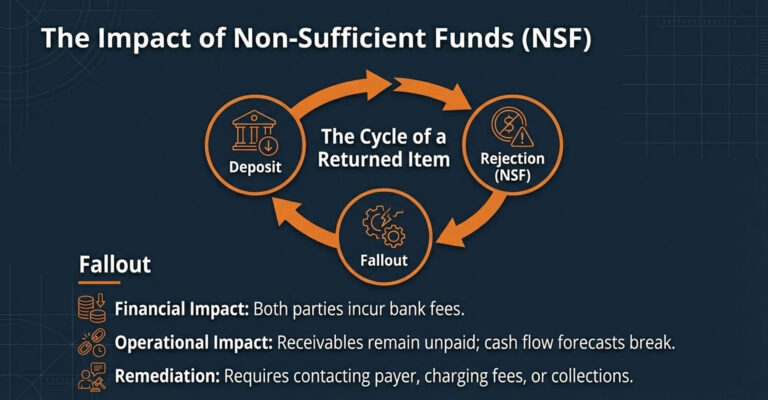

Non-Sufficient Funds and Returned Checks

NSF (non-sufficient funds) checks bounce when the payer’s account lacks adequate funds. The recipient typically incurs bank fees, loses the expected payment, and faces the administrative burden of pursuing collection.

Check Fraud and Forgery

Fraudsters may alter check amounts, forge signatures, or create counterfeit checks that appear legitimate. 63% of businesses experienced check fraud in 2024. For large payments, verifying authenticity with the issuing bank before deposit can prevent significant losses.

Stop Payment Orders

Payers can instruct their bank to refuse payment even after issuing a check. While stop payments have legitimate uses, they leave recipients with limited recourse if a payer acts in bad faith.

Stale-Dated and Expired Checks

Banks typically consider checks “stale-dated” after six months and may refuse to honor them. Recipients who delay deposits risk having to request replacement checks.

What Happens When a Check Bounces

What happens when a check payment bounces and how do businesses respond?

A bounced check—also called a returned check or NSF check—occurs when the payer’s account lacks sufficient funds. The recipient’s bank notifies them of the return, typically within a few days of the original deposit.

Both parties usually incur bank fees: the payer faces an overdraft or NSF fee, while the recipient pays a returned item fee. More significantly, the recipient’s accounts receivable balance remains unpaid.

Businesses can pursue several remedies: contacting the payer to request replacement payment, charging returned check fees as specified in contracts, or escalating to collections for persistent non-payment.

Best Practices for Managing Check Payments

How can finance teams manage check payments efficiently?

With proper processes in place, businesses can reduce the risks and administrative burden associated with check payments.

1. Verify Check Authenticity Before Deposit

For large payments, inspect checks for security features like watermarks and microprinting. Confirm payer information matches your records, and consider calling the issuing bank to verify funds for amounts above a certain threshold.

2. Establish Clear Payment Terms and Policies

Document accepted payment methods, returned check fees, and payment deadlines in contracts and on invoices. When customers understand the consequences of bounced checks upfront, disputes become less common.

3. Automate Cash Application and Reconciliation

Modern AR platforms can match check payments to open invoices using customer and amount data, reducing manual data entry and errors. Even businesses that receive significant check volume can streamline their processes with the right tools.

4. Implement Internal Controls for Check Handling

Segregate duties so that the person receiving checks differs from the person depositing them. For high-volume operations, lockbox services route payments directly to a bank processing center, improving security and speed.

5. Encourage Transition to Electronic Payments

Offer ACH, credit card, and online payment options alongside checks. Some businesses incentivize electronic payments through convenience or small discounts, gradually shifting their payment mix toward more efficient methods.

Check Payments vs ACH and Wire Transfers

How do check payments compare to ACH and wire transfers?

Businesses often choose between checks, ACH transfers, and wire transfers based on speed, cost, and transaction requirements.

Many businesses transitioning away from checks adopt ACH for recurring billing because it combines low cost with reasonable speed. Checks remain relevant when payers lack bank account information for electronic transfers or when recipients prefer paper documentation.

| Factor | Check Payment | ACH Transfer | Wire Transfer |

|---|---|---|---|

| Speed | 2-5 business days | 1-3 business days | Same day or next day |

| Cost to Sender | Check stock, postage ($2.01-$4.00 total) | Low or free | Higher fees ($15-50) |

| Cost to Recipient | Free to deposit | Low or free | May incur fees |

| Reversibility | Can be stopped or bounce | Reversible (limited window) | Generally irreversible |

| Best For | B2B invoices, paper-preferring vendors | Recurring payments, payroll | Large, time-sensitive payments |

How to Streamline Check Payment Processing with AR Automation

How can AR automation reduce the burden of check payment processing?

For businesses that still receive significant check volume, AR automation platforms offer a path to efficiency without requiring customers to change their payment habits.

AR automation platforms integrate with lockbox services to receive remittance data electronically, eliminating manual mail processing. They auto-match payments to open invoices using customer identifiers and amount data, flagging discrepancies for review rather than requiring line-by-line reconciliation.

Once payments are matched, the system posts journal entries automatically, updating AR balances and cash accounts without manual intervention. Ordway’s Accounts Receivable Automation supports check payments alongside ACH, cards, and wires, providing a unified view of all payment activity with automated cash application.

Frequently Asked Questions about Checks

How long does it take for a check payment to clear?

Most checks clear within two to three business days, though banks may hold funds longer for large amounts, new accounts, or out-of-state checks. Regulation CC sets maximum hold periods, but actual availability varies by bank.

Do checks expire if not deposited?

Banks typically consider checks “stale-dated” after six months and may refuse to honor them. Recipients who wait too long often need to request a replacement from the payer.

Can businesses accept check payments for recurring billing?

Yes, though checks require manual processing each billing cycle, making them less efficient than auto-pay methods like ACH or credit cards. For subscription and recurring revenue models, electronic payment methods significantly reduce administrative overhead.

How do you void a check payment?

Write “VOID” in large letters across the front of the check to prevent it from being cashed. Record the voided check number in your records for reconciliation purposes.

What is the difference between a check and a cheque payable?

“Check” and “cheque” refer to the same payment instrument. “Check” is the American English spelling, while “cheque payable” is the British English term used in the UK, Canada, Australia, and other Commonwealth countries.